Rethinking Defense for the Digital Age

Summary

This report examines the profound transformation underway in US defense sector, driven by technology, venture capital, and policy shifts, and why startups must play a central role. It highlights how inefficiencies in defense procurement create market gaps, the rise of dual-use technologies, and the strategic importance of artificial intelligence (AI), autonomous systems, and space- based defense technologies. The report provides a roadmap to capitalize on the defense sector’s growing reliance on private-sector innovation, positioning VC-backed start-ups at the forefront of the next era of national security.

Executive Summary

The US defense sector is undergoing its most profound transformation since the 1950s, as technology, venture capital, policy shift, and geopolitical urgency converge to redefine military strategy. While established defense contractors continue to play a pivotal role, policy shifts under the new administration are likely to accelerate the integration of venture-backed startups into the defense ecosystem. This report examines the burgeoning opportunities for early-stage investors within this evolving defense landscape.

Despite the Pentagon’s growing reliance on private-sector innovation, many startups fail to navigate the complexities of defense procurement, while the Pentagon struggles to onboard non-traditional vendors at scale. This creates a market inefficiency where high- impact technologies remain underutilized, leaving room for investors to back startups that can bridge this gap. While the Department of Defense (DoD) has taken proactive steps to address this through mechanisms like the Other Transaction Authority (OTA) agreements, the pace of adoption must accelerate to meet the urgency of modern defense needs. The report highlights the massive opportunity in dual- use technology startups. While venture-backed firms are at the forefront of AI, autonomy, cybersecurity, and space technologies, only a fraction have entered the defense market. The report argues that aligning early with DoD priorities allows startups to access government contracts, secure non-dilutive funding, and de-risk their commercial models by diversifying into defense.

The report further highlights the critical importance of space as an emerging warfighting domain, underscored by the establishment and substantial funding of the US Space Force (USSF). The USSF’s budget has doubled from $15 billion in 2021 to $29 billion in 2024, reflecting a strong commitment to advancing space-based defense capabilities. Foreign military sales (FMS) requests for US space capabilities have increased sixfold in 2024, highlighting the growing role of space systems in both economic and national security. This focus has led to increased investments in space-based defense technologies, such as autonomous satellites and advanced missile detection systems.

It also advocates for a shift away from inefficient legacy spending as the defense sector struggles under the weight of rising costs, bureaucratic inertia, and the growing need for faster innovation cycles. By leveraging advancements in AI, autonomous systems, and cybersecurity, the new-age start-ups can provide superior capabilities at reduced costs. The DoD’s collaboration with firms like Anduril, Shield AI, and Skydio reflects this strategic pivot.

The report underscores the ascendancy of algorithmic warfare, where dominance is determined by the capacity to process and act upon data with unprecedented speed and accuracy. The Pentagon’s Joint All-Domain Command and Control (JADC2) initiative is laying the groundwork for a hyper-connected battlefield, where AI-driven analytics and autonomous systems coordinate seamlessly across land, sea, air, space, and cyber domains. Startups developing AI-driven threat detection, unmanned systems, and advanced cybersecurity are positioned for significant defense contracts.

The defense sector is a highly attractive market — both well-funded and resilient. However, for startups to succeed, they must overcome procurement challenges, align with DoD priorities, and actively engage with the defense ecosystem.

Key Points

VCs Have Massive Opportunity in Dual-Use Tech Start-ups: As modern warfare and national security increasingly rely on AI, autonomous systems, cybersecurity, and space technologies, the demand for Dual-Use innovations—solutions applicable to both civilian and military domains—is surging. An analysis of NATO and allied countries by Mind the Bridge, a global open innovation platform, reveals that while pure defense-tech scaleups remain scarce (with fewer than 200 companies—just 0.3% of the 60,000 total tech startups), the landscape shifts dramatically when considering Dual-Use technologies, where 15,000 scaleups (25% of VC-backed tech firms) are developing solutions that could serve both markets. Despite this potential, only 5-6% (700+) of these dual-use companies have formally expanded into defense. By comparison, Israel boasts a 60% conversion rate, demonstrating a 10x growth opportunity for other regions. This gap highlights a clear market inefficiency—many startups may be overlooking defense applications, while governments struggle to onboard non-traditional vendors at scale. For startups, the opportunity is twofold: access to government contracts and funding, as well as the chance to de-risk commercial models by diversifying into defense.

Space is the Warfighting Domain of the Future: Space is now firmly established as a critical warfighting domain, with the USSF emphasizing the growing threat posed by the Chinese and Russian anti-satellite (ASAT) capabilities. In response, the US is accelerating investments in space-based defense through OTA-enabled projects, which are fast-tracking advancements in space situational awareness, resilient satellite communications, and potential space-based weapons systems. Also, the USSF’s budget has surged from $15.4 billion in 2021 to $30.3 billion in 2024, reflecting the US’ commitment to orbital deterrence and operational readiness.

VC-Backed Start-ups Need to Align Their Innovations with the DoD’s Needs from the Outset: VC-backed start-ups must focus on aligning their innovations with the DoD’s needs from the outset to navigate the complex defense contracting landscape. The DoD has outlined 14 critical technology areas, such as quantum science and AI, which start-ups should target to meet national security priorities. Only 16% of DoD Small Business Innovation Research (SBIR)-funded companies receive Phase III contracts (commercialization stage contracts), and less than 1% of Phase I awardees achieve Program of Record (POR) status, according to data from JP Morgan. This highlights the “Valley of Death” challenge, where start-ups struggle to move from initial funding to commercialization, underscoring the need for early alignment.

Traditional Defense Models are Failing Under Rising Costs and Global Threats: The US spends an estimated $100 billion annually on maintaining outdated and ineffective legacy systems against modern threats. This expenditure diverts funds from investing in innovative technologies that could provide better capabilities at lower costs. The US has no choice but to shift DoD budgets away from incumbents and toward startups. Startups often operate with leaner business models, allowing them to develop innovative soluti lower costs compared to traditional defense contractors. For example, AI-driven logistics solutions could reduce supply chain costs by up to 20-30%, translating into savings of approximately $10 billion annually if implemented across various military operations.

Overview

The US defense industry is a complex network of organizations, facilities, and resources that provides the US government with defense-

related products, services, and materials. The industry is made up of a variety of entities, including:

- Private defense firms: These firms produce weapons, and include the “big five” of Lockheed Martin, Boeing, General Dynamics, RTX (formerly Raytheon), and Northrop Grumman.

- Not-for-profit research centers and university laboratories: These institutions are part of the defense industrial base.

- Government-owned industrial facilities: These facilities are part of the defense industrial base.

Big Five” alone routinely split more than $150 billion in Pentagon contracts annually, or nearly 20% percent of the total Pentagon budget.

Military-Industrial Complex Through Time

The history of the military-industrial complex can be understood in distinct eras, each marked by shifts in government reliance, industrial innovation, and defense strategies.

The First Era relied on civilian industries during wartime, a reactive approach that lasted until World War II. During the 1940s, arms production in the US skyrocketed from 1% to 40% of GDP, transforming the defense landscape. This marked the start of the Second Era, where a robust military-industrial complex emerged. The Cold War fueled a boom in defense contracting, leading to groundbreaking innovations like jet engines and early computers—many of which had transformative civilian applications. The defense industry became deeply intertwined with the US economy, with its success tied to a handful of dominant contractors.

The collapse of the Soviet Union in the 1990s ushered in the Third Era, a period of consolidation and complacency. With no existential threats, major contractors focused on maintaining dominance through lobbying and legacy contracts, sidelining innovation.

However, the early 2000s brought disruption. The rise of the internet, the global spread of the Information Age, and the events of September 11, 2001, underscored the need for agility. Startups began developing cutting-edge technologies that often outperformed legacy defense systems. In response, the "Third Offset Strategy,” emphasizing investments in autonomous systems, robotics, and advanced manufacturing.

For the US, NATO, and allied nations, the integration of AI is imperative for preserving their traditional technological edge. Whether in autonomous systems, predictive warfare, or ethical frameworks for future conflicts, AI’s potential to revolutionize defense operations underscores its critical role in maintaining global security and stability.

Inefficiencies in the Current Defense Business Model

The National Defense Industrial Strategy highlights the critical need to fortify the connection between a robust defense industrial base and the United States’ military strength. However, the perspectives of defense-tech companies remain largely underrepresented in this dialogue.

In 2014, the Defense Department recognized the growing need to access advanced technologies from commercial partners due to declining government-led research and development. Over the past decade, the department has made strides in bridging this gap by creating organizations such as the Defense Innovation Unit, AFWERX, Army Applications Lab, and NavalX, along with programs like the Rapid Defense Experimentation Reserve and Accelerate the Procurement and Fielding of Innovative Technologies. These initiatives have streamlined access to cutting-edge technologies for defense personnel, attracting commercial companies and investors to the defense sector.

While these efforts have significantly improved the ease of collaboration and funding opportunities for companies, critical obstacles persist. Overcoming these challenges is vital to ensure sustained innovation and the integration of transformative technologies into US defense capabilities.

The US defense industry finds itself at a critical inflection point, where its current business model is increasingly unsustainable in the face of asymmetric threats and evolving technologies. For example, intercepting low-cost Houthi drones—built for a few thousand dollars—required US naval missiles costing up to $2.1 million per shot. This imbalance highlights the urgent need for a technological shift.

Evolution of DoD Policy and Role of AI in Modern Warfare

The DoD has consistently evolved its policies to address the shifting demands of modern warfare, and AI now stands at the forefront of this transformation. While AI’s application in military operations remains in its infancy, its current contributions are already redefining battlefield dynamics and decision-making processes.

One of AI’s most impactful roles lies in information gathering and processing—tasks previously limited by human capacity. Military operations generate immense volumes of data from satellite imagery, surveillance feeds, and communication signals. In the past, analyzing these vast datasets required significant manpower and time, often delaying actionable insights. Today, AI systems can sift through terabytes of data, identify patterns, and flag critical information in seconds, providing real-time intelligence that enhances situational awareness for warfighters.

A prime example of AI’s growing utility is in threat identification and recognition, particularly in air combat. Traditionally, identifying enemy aircraft required the coordination of numerous sensors and the expertise of specialists analyzing hours of data. AI now performs these tasks with unparalleled speed and precision. By analyzing unique radio or radar signals emitted by aircraft, AI systems can pinpoint enemy assets almost instantaneously. What once required the effort of teams working over days or weeks can now be accomplished in milliseconds, offering a decisive edge in combat scenarios.

Deployed AI Solutions by DoD

Established firms such as Boeing, General Dynamics, Lockheed Martin, Raytheon, and Northrop Grumman, alongside emerging players like Anduril, are integrating AI across a range of military applications, from logistics and surveillance to combat systems and autonomous technologies.

The DoD is aggressively integrating AI to maintain a strategic edge in national security. With over 685 AI-related projects under its purview, the DoD has significantly ramped up investments, allocating $1.8 billion for AI in the FY2025 defense budget. Central to this effort is the Chief Digital and AI Office (CDAO), which oversees AI adoption across applications like autonomous systems, predictive maintenance, and battlefield decision-making.

Startups play a critical role in this ecosystem, with venture-backed companies such as Shield AI, Anduril Industries, and Rebellion Defense leading innovation in autonomous drones, AI-powered decision-making software, and uncrewed systems. Shield AI’s Hivemind platform, for instance, enables autonomous operations for drones and fighter jets even in contested environments. Similarly, Palantir has partnered with Enabled Intelligence to improve AI model accuracy through high-quality data labeling. These collaborations underscore the DoD’s reliance on public-private partnerships to accelerate AI deployment despite fiscal constraints.

Trends in Militarization: A Paradox of Modern Warfare

Global militarization presents a paradox: while traditional metrics like troop size and defense spending as a percentage of GDP have declined, the intensity of conflicts has surged. Nations are shifting from manpower-heavy defense strategies to technologically advanced systems, investing in AI, autonomous systems, space-based capabilities, and hypersonic weapons.

France, for example, reduced its military size from 500,000 in 1995 to 300,000 in 2020, further downsizing its African presence while boosting defense tech funding from $27M to $43M by 2025. France is also enhancing its space and maritime defense, developing autonomous underwater vehicles and deploying military satellites.

China, historically reliant on mass military forces, cut 1.6 million troops between 1995 and 2020 while advancing its hypersonic missile capabilities (DF-17), nuclear arsenal, and AI-driven military systems.

The UK faces recruitment shortfalls, with its armed forces missing their personnel target by 5,440 in 2024. To compensate, it prioritizes high-tech defense solutions like the F-35 fighter, submarine warfare, and laser weaponry (DragonFire).

Meanwhile, Russia’s military declined from 1.9 million in 1992 to 1.4 million in 2020, struggling with recruitment due to economic and demographic issues, exacerbated by casualties in Ukraine. Western sanctions have further restricted its access to advanced defense technology, though Putin aims to expand military personnel to 1.5 million. This global transition underscores the growing dominance of technology in modern warfare.

Countries no longer rely on large standing armies but on precision capabilities, cyber warfare, and strategic deterrence, fundamentally reshaping how conflicts are fought. While the size of militaries shrinks, defense spending is increasingly directed toward next-generation warfare, ensuring that technological superiority—not sheer numbers—defines military power in the 21st century. This shift highlights a new era of conflict where intelligence-driven, high-tech capabilities dictate the balance of global security.

Key Reports Takeaways

VCs Have Massive Opportunity in Dual-Use Tech Start-ups

As modern warfare and national security increasingly rely on AI, autonomous systems, cybersecurity, and space technologies, the demand for Dual-Use innovations—solutions applicable to both civilian and military domains—is surging. An analysis of NATO and allied countries by Mind the Bridge, a global open innovation platform, reveals that while pure defense-tech scaleups remain scarce (with fewer than 200 companies—just 0.3% of the 60,000 total tech scaleups), the landscape shifts dramatically when considering Dual-Use technologies, where 15,000 scaleups (25% of VC-backed tech firms) are developing solutions that could serve both markets. Despite this potential, only 5-6% (700+) of these Dual-Use companies have formally expanded into defense. By comparison, Israel boasts a 60% conversion rate, demonstrating a 10x growth opportunity for other regions.

This gap highlights a clear market inefficiency—many startups may be overlooking defense applications, while governments struggle to onboard non-traditional vendors at scale. For startups, the opportunity is twofold: access to government contracts and funding, as well as the chance to de-risk commercial models by diversifying into defense.

The “valley of death” represents a critical transition gap in the defense acquisition process where promising technologies struggle to advance from early-stage development to full-scale deployment and integration. This phenomenon creates significant challenges for startups attempting to do business with the DoD (DoD). According to the Defense Acquisition University, this period typically stretc s

1-2 years, during which startups face severe cash flow constraints while navigating the government’s complex procurement timeline.

The core problem stems from a fundamental misalignment: acquisition officials demand higher technology maturity levels than science and technology departments are willing to fund, creating a dangerous gap where promising innovations often flounder and fail.

The Financial Reality for Defense Startups

For defense-focused startups, understanding burn rate and runway metrics becomes critically important for survival. Unlike typical commercial startups that might operate with 8–10-month runways, defense entrepreneurs need significantly longer financial runways due to extended government procurement timelines. The standard runway calculation (cash reserves divided by monthly burn rate) takes on heightened importance in this sector

Financial planning for defense startups requires careful calibration. At the product development stage, Fred Wilson’s guidelines suggest maintaining gross burn rates up to $50,000 monthly, while the business building stage may require up to $250,000 monthly burn. However, defense startups often need to plan for extended periods without significant revenue while government contracts progress through evaluation phases. This requires meticulous cash management and strategic fundraising approaches to extend runway through the valley of death period.

The Dual-Use Imperative

Implementing a dual-use business model represents perhaps the most effective strategy for navigating the valley of death. This approach involves developing technologies with both commercial and defense applications, creating multiple revenue streams that can sustain operations during protracted government procurement cycles. The historical success of this model is evident in technologies like GPS, which began as purely military innovations but eventually enabled commercial giants like Google Maps, Uber, and Instacart to build billion-dollar enterprises.

The dual-use strategy provides critical advantages: commercial market sales cycles typically run 3-6 months versus DoD’s 12-24 months, generating essential cashflow during government procurement delays. Furthermore, commercial feedback loops accelerate product development and validation, making the technology more mature and attractive to defense customers. This approach transforms the valley of death from an insurmountable obstacle into a manageable financial challenge by diversifying revenue sources and reducing dependence on government contracts alone.

Venture-Backed Startups Will Disrupt Defense Contracting

The US now boasts over 1,000 venture-backed startups developing “smarter, faster, and cheaper” defense technologies, signaling a seismic shift in the defense contracting landscape. Unlike traditional primes burdened by legacy systems and bureaucratic inertia, these startups bring agility, rapid innovation, and cost efficiency—qualities increasingly crucial for modern warfare.

Venture-backed startups are poised to disrupt the defense contracting landscape by introducing agility, innovation, and cost efficiency that traditional defense primes struggle to match. Over the past decade, venture capital investment in defense tech has grown 18-fold, from $1.9 billion in 2014 to $35.8 billion in 2023, with a significant portion directed toward dual-use technologies like AI and autonomous systems.

Over the past two decades, national security agencies have increasingly turned to non-traditional firms for technological innovations, leading to three distinct waves of defense tech startups:

1. First Wave (Early 2000s): Pioneering companies like SpaceX and Palantir emerged, developing technologies initially aimed at sectors outside the DoD (DoD).

2. Second Wave (Mid-to-Late 2010s): Startups such as Anduril and Shield AI adapted commercially derived technologies for defense applications, introducing innovations like autonomous systems and AI-driven surveillance tools.

3. Third Wave (Early 2020s to Present): An expanding ecosystem of startups and non-traditional companies is driving innovation, attracting significant venture capital, and aiming to scale operations to meet evolving defense needs.

Space is the Warfighting Domain of the Future

Geopolitical competition is expanding beyond Earth. After decades of US dominance in space following the Cold War, that control is now being challenged. Just as major powers compete for influence in the South China Sea and the Arctic, they are now pushing their ambitions into space—the next critical battleground.

Space activity falls into three main categories: civil, national security, and commercial. In national security, space assets are crucial for intelligence gathering, arms control verification, and military operations. The US relies on satellites in geostationary orbit (GEO) for early warning and nuclear threat detection, while those in low Earth orbit (LEO) support real-time military coordination. But with new players rapidly expanding their capabilities, the US no longer enjoys uncontested dominance in space.

Space is now firmly established as a critical warfighting domain, with the USSF emphasizing the growing threat posed by the Chinese and Russian ASAT capabilities. In response, the US is accelerating investments in space-based defense through OTA-enabled projects, which are fast-tracking advancements in space situational awareness, resilient satellite communications, and potential space-based weapons systems. Also, the USSF’s budget has surged from $15.4 billion in 2021 to $30.3 billion in 2024, reflecting the US’ commitment to orbital deterrence and operational readiness.

US Space Assets Face Rising Threats from China, Russia, and Other Adversaries

The US maintains a leading position in space with a vast array of operational satellites, including advanced geostationary (GEO) satellites dedicated to arms control verification, nuclear attack warnings, and intelligence gathering. However, these critical national security and commercial assets are increasingly at risk. Both China and Russia have developed capabilities to disrupt or destroy these satellites through various means, such as electronic warfare, direct-ascent ASAT missiles, directed energy weapons, and potentially space-based kinetic systems.

In response to these threats, the US has begun deploying a larger number of smaller satellites in diverse orbits to mitigate risks. Despite these efforts, the pace of US countermeasures has not kept up with the evolving threats.

Russia’s Immediate Threats

Russia’s actions pose immediate dangers to existing satellites. Notably, in November 2021, Russia conducted a direct-ascent ASAT test, destroying one of its own satellites and creating a significant debris field in LEO. This event generated over 1,500 pieces of trackable debris, endangering other space assets.

Additionally, just before its 2022 invasion of Ukraine, Russia executed a cyberattack on Viasat, a US company providing satellite communications to Ukraine. This attack disrupted internet access for thousands of users across Europe, highlighting the vulnerability of space-based communication systems to cyber threats.

There are also concerns about Russia’s potential intentions to deploy nuclear weapons in space, which would violate international treaties and pose catastrophic risks to satellites, especially those in LEO. Such actions could lead to widespread disruptions and escalate global tensions.

China’s Strategic Ambitions

China’s approach presents a long-term challenge, aiming to not only threaten current space assets but also to contest US leadership in space. China is rapidly advancing its counterspace capabilities, including the development of ASAT weapons and other technologies designed to neutralize US space advantages. This strategic buildup indicates China’s intent to challenge US dominance in space, potentially leading to a new era of geopolitical competition beyond Earth’s atmosphere.

China’s commercial space sector is rapidly expanding, bolstered by substantial state support. The China Satellite Network Group is developing the Guowang constellation, a planned network of 13,000 satellites designed to rival Starlink. Meanwhile, Shanghai Spacecom Satellite Technology has secured nearly $1 billion in funding for its G60 constellation, another large-scale satellite initiative. In August 2024, the state-owned China Aerospace Science and Technology Corporation (CASC) successfully launched the first 18 satellites for the project, marking a significant step toward establishing a global satellite network.

Much like its advancements in electric vehicles, China’s space industry benefits from aggressive government investment and strategic industrial planning. Beyond communications, China’s space ambitions may extend to resource extraction. Some analysts see its lunar soil sample missions as early steps toward future Moon mining operations, signaling broader economic and geopolitical aspirations in space.

The Growing Challenge of Space Traffic Management

The safe and sustainable use of space is becoming an increasingly urgent concern. Modern society depends on satellites for everything from communications and navigation to weather forecasting and national security. However, as space becomes more congested, the risk of collisions and cascading debris events—known as the Kessler Effect—grows exponentially.

First predicted by NASA scientist Donald Kessler in 1978, this phenomenon describes a scenario in which the rising number of objects in orbit leads to a chain reaction of collisions, generating debris that further endangers satellites and human spaceflight. Half a century later, this challenge is no longer theoretical.

Today, space is more crowded than ever. There are 36,000 objects larger than 10 cm in orbit, 30,000 of which are well-documented and cataloged with known trajectories. The remaining 6,000 unreferenced objects include military assets and debris too difficult to track continuously. In recent years, an additional 12,000 objects have been introduced into Earth’s orbital environment, further straining space traffic management systems.

International Treaties and Potential Violations

The deployment of nuclear weapons in space would contravene key international agreements, notably the 1967 Outer Space Treaty, which prohibits the placement of nuclear weapons in orbit. Despite these legal frameworks, the actions of US adversaries suggest a growing willingness to challenge established norms, both on Earth and in space. Such developments underscore the need for robust international dialogue and updated policies to address the evolving security landscape in space.

Space Force Leans on Start-ups

VC-backed agreements play a critical role at Space Force as it pursues new ways of securing space as both a warfighting domain and critical infrastructure that supports the US’ overall economy. Space Force is leveraging multiple mechanisms to engage with VC-backed start-ups, primarily through the Space Enterprise Consortium (SpEC) and the Small Business Innovation Research (SBIR) program. SpEC, established in 2017 under the Air Force Space and Missile Systems Center and now managed by the National Security Technology Accelerator (NSTXL), is an OTA vehicle designed to bridge the cultural gap between military buyers and commercial space start-ups. This initiative allows for rapid prototyping and flexible contracting, with SpEC overseeing up to $12 billion in awards over 10 years for space-related projects, reducing contract award timelines by 36% and growing membership to 441 by 2020. This approach minimizes barriers for small, non-traditional businesses, enabling them to compete for federally funded space prototype projects and fostering innovation in areas like space situational awareness and satellite communications.

The SBIR program, managed through SpaceWERX, the innovation arm of the Space Force, further facilitates engagement by awarding contracts to start-ups to explore technological potential and commercialize innovations. In August 2021, the Space Force awarded $32 million in SBIR Phase 2 contracts to 19 companies, each receiving $1.7 million, following a virtual pitch event that marked the launch of SpaceWERX. These contracts focus on technologies like positioning, navigation, and timing (PNT), cybersecurity, and satellite maneuvering, aligning with the Space Force’s mission to deter and win wars in space.

AI Will Transform Defense by Enabling Algorithmic Warfare

AI is transforming defense through algorithmic warfare, enabling faster decision-making, enhanced precision, and operational efficiency. AI-powered autonomous drones, such as those developed under the US Air Force’s Skyborg project, perform reconnaissance and targeted strikes without human intervention, reducing risks to personnel and increasing mission effectiveness.

The US government has dramatically ramped up its investment in AI, with federal spending on AI-related contracts soaring over the past year—largely fueled by military priorities. The potential value of AI-focused federal contracts surged by nearly 1,200%, jumping from $355 million in the year leading up to August 2022 to $4.6 billion in the same period before August 2023.

DoD drove this surge which significantly escalated its commitment to AI-powered capabilities. The DoD’s allocated funding for AI-related contracts nearly tripled, rising from $190 million to $557 million over the same timeframe. This sharp increase underscores the Pentagon’s growing recognition of AI as a critical enabler of next-generation warfare, from autonomous weapons and battlefield intelligence to cybersecurity and logistics optimization.

The next frontier of defense superiority will be defined by algorithmic warfare — the ability to process, predict, and execute at machine speed. The Pentagon’s JADC2 initiative aims to fuse sensor data across land, air, sea, space, and cyber domains, creating a real-time battlefield intelligence network. AI will move beyond decision support and into autonomous execution, where self-learning algorithms will optimize force deployment, counter cyber threats preemptively, and autonomously coordinate swarms of unmanned systems.

AI DSS: A Necessity in Electromagnetic Warfare

AI is becoming a critical asset in the Russia-Ukraine conflict, helping analyze vast amounts of data from multiple sources to enhance decision-making. Ukraine leverages AI to gain an advantage over Russian forces. This technological edge is driven by collaboration between the Ukrainian government and the private sector, with Western allies providing key AI tools. As evident in this conflict, there is a rise in Electromagnetic Warfare (EW), a type of warfare that uses energy, like radio waves or microwaves, to disrupt or damage an enemy’s electronic systems, such as radar, communication devices, or sensors. There are three main actions in EW:

• Jamming: This involves sending out interference signals to block or confuse an enemy’s communication or radar systems, making it harder for them to track or communicate effectively.

• Spoofing: This tricks the enemy by sending fake signals that appear to be from their systems, leading them to make wrong decisions or misinterpret information.

• Cyber Attacks: This includes hacking into enemy systems to take control or disable their electronic devices, such as GPS or communication networks.

AI DSS is vital in tackling EW. For instance, US drone startups have struggled against Russia’s EW tactics, particularly GPS jamming, as reported by the Wall Street Journal. Modern warfare demands AI-powered drones and weapons that can operate independently of human control or networks. Shield AI’s drones have performed better in Ukraine, as they don’t rely on GPS, according to co-founder Brandon Tseng.

The US government is actively supporting such emerging technologies. In 2023, the US DoD released the National Defense Science and Technology Strategy (NDSTS), emphasizing the use of critical technologies like quantum science, AI, autonomy, and space tech to strengthen national security.

Shield AI, a California-based startup, is developing Hivemind, an AI system that enables autonomous operation of drone and aircraft swarms without GPS, communication, or a pilot. Its partnerships with the US DoD and major defense contractors like Boeing, Textron Systems, and Northrop Grumman ensure steady revenue and enhance credibility. Similarly, Anduril, another California startup, delivers autonomous systems powered by its Lattice OS, ensuring integrated security and situational awareness across land, sea, and air. Its adoption by the US DoD, as well as Australian and UK defense ministries, ensures steady revenue. Massachusetts-based Merlin Labs is transforming human piloting into software, with its Merlin Pilot having logged over 800 hours on 500 missions across five aircraft types. These startups are positioned to disrupt modern warfare and evolve into highly valuable companies.

Case Study: Impact of AI DSS in the Two Major Wars of Current Times\

The military use of AI, once theoretical, is now a reality in Gaza and Ukraine. Both conflicts focus on decision support, intelligence analysis, and targeting, with AI enabling faster data processing. Ukraine uses AI against a larger opponent, while Israel leverages it to strengthen its military against Hamas. These cases offer valuable insights and cautionary lessons for other forces regarding AI’s role in tactical, operational, and strategic operations.

Gaza: The Israel Defense Forces (IDF) utilize an AI system called ‘Lavender’ to identify Hamas commanders with 90% accuracy, drawing from a database of 37,000 Palestinians, as reported by +972 Magazine and Local Call. The IDF has reportedly accepted 15 to 20 civilian casualties as collateral for each junior Hamas commander targeted. Although the Israeli government denies these claims, this technology offers a glimpse into the future of warfare. Beyond data processing and intelligence, Israel employs AI to track Hamas militants hiding in Gaza’s 1,300 tunnels, spanning over 310 miles. The IDF uses AI-equipped drones, including those developed by Israeli startup Robotican, to detect humans and operate underground. Additionally, the IDF deploys an AI model, ‘Gospel’, which identifies high priority bombing targets. During the 11-day war with Hamas in May 2021, Gospel generated 100 targets per day, a significant increase from the previous rate of 50 targets per year, per Aviv Kohavi, former chief of IDF.

Ukraine: Since the onset of the war with Russia, Ukraine’s military has been using Palantir’s Gotham system, an AI-powered decision-making platform known as the ‘AI-powered kill chain.’ This system integrates various data sources—such as images, drone footage, and battlefield data—into an operational map, enhancing situational awareness and operational control. The Prosecutor General’s Office is also collaborating with Palantir to process data related to nearly 80,000 war crimes committed by Russia. Clearview AI, a New York-based facial recognition software startup, was involved in identifying participants in the US Capitol attack on January 6, 2024, analyzing open-source data like social media images to match individuals with existing profiles. The technology has been used by 18 Ukrainian government agencies to investigate war crimes, identify deceased soldiers, detect infiltrators, and improve checkpoint security. In 2023, it helped locate 150 orphans in Crimea who were at risk of being deported to Russia, as well as identify captured Ukrainians and those involved in child abductions. Moreover, Ukraine is also using AI-powered drones that have a hit rate of roughly 80%, significantly above the hit rate of 30-50% of manually controlled drones.

Role of AI DSS in the Fifth Domain of Warfare

The surge in cyber sabotage and espionage has accelerated cyber militarization, with many countries now recognizing ‘cyber’ as the fifth domain of warfare, alongside land, sea, air, and space. Significant budgets are being allocated to strengthen military cyber capabilities, incorporating both offensive and defensive strategies. Nearly 50 nations either possess or are developing offensive cyber capabilities.

Technologies like data labeling and cybersecurity are critical for national security. Scale AI, though not a traditional defense tech company, enhances defense applications by integrating AI into existing defense hardware. This reduces cognitive load for operators, improves sensor intelligence, and lowers maintenance costs. An 89% valuation markup in the latest funding round affirms investor confidence.

In 2023, the US Cybersecurity and Infrastructure Security Agency partnered with SentinelOne to launch the Joint Cyber Defense Collaborative, aimed at strengthening cybersecurity for the US government and critical infrastructure. With adversaries using AI to target vital systems, AI-powered defense is crucial. AI-driven cybersecurity startups like Cyera are key to addressing national security threats. Based in New York, Cyera offers a cloud-native, agentless platform that secures data across diverse environments. Cyera’s 180% valuation increase in its latest funding round highlights strong investor confidence in its growth potential.

Favorable Regulatory Tailwinds to Boost AI DSS Adoption

In 2024, the US DoD has requested a record $145B RDT&E budget, marking a 4% increase over 2023. This includes $1.8B for AI, focusing on responsible AI/ML capabilities, secure platforms, workforce development, and DoD-wide data management and modernization. Additionally, The Congressional Budget Office projects that military spending will increase by 10% between 2028 and 2038, adjusted for inflation.

Additionally, the US Army is reducing its force by approximately 24,000 personnel, or nearly 5%, as part of a broader restructuring aimed at enhancing readiness for future conflicts. This shift reflects a strategic pivot from manpower expansion to technological advancement, emphasizing future large-scale combat scenarios. These changes align with a focus on minimizing direct combat, incorporating advanced technologies such as AI DSS and AI-powered UAVs into the military arsenal.

AI DSS to Support the US Deliver Security Commitments to Allies

The United States contributes 15.9% of NATO’s budget and holds the largest defense spending within the alliance. Integrating AI DSS can substantially reduce this financial burden through advanced data analysis and decision-making capabilities.

Traditional Defense Models are Failing Under Rising Costs and Global Threats

The current defense industrial base, built around lengthy development cycles and rigid bureaucratic structures, struggles to adapt quickly enough to modern warfare demands. These systems are burdened by overhead, outdated technology, and inefficient processes that inflate costs and delay innovation. With defense budgets ballooning and strategic challenges intensifying, the status quo risks eroding the US military’s readiness and operational effectiveness.

To address these issues, a fundamental shift is needed. Tech start-ups offer a nimble, cost-effective alternative to traditional defense contractors. Agile companies—driven by rapid innovation in AI, robotics, and autonomous systems—are already proving capable of delivering breakthrough solutions, from advanced surveillance platforms to counter-drone technologies. By integrating these start-ups into the national defense strategy, the US can inject fresh innovation, accelerate development cycles, and create a more adaptive and resilient military posture that meets the complex challenges of the 21st century.

The Burden of Legacy Systems

The US DoD spends a substantial amount on maintaining legacy systems that are often outdated and less effective against modern threats. These systems, such as the B-52 bomber (in service since the 1950s) and the Bradley fighting vehicle (since the 1980s), require continuous and costly maintenance. The DoD’s FY2023 operations and maintenance (O&M) budget stood at $339 billion, with projections of reaching $361 billion by FY 2029. Much of this spending diverts resources from developing new technologies that could offer better capabilities at lower costs.

The start-ups are well-positioned to address critical capability gaps in the US defense. Elon Musk has also criticized legacy defense technologies, such as manned fighter jets like the F-35, calling them obsolete and advocating for drones due to the F-35’s complexity and high costs. For reference, in the ongoing Ukraine conflict, both sides have deployed tens of thousands of small commercial drones. Consumer quadcopters, priced under $2,000, have shown prominence in tactical reconnaissance, artillery targeting, and bomb delivery. Moreover, first-person view (FPV) drones, costing just $400, are shown prowess in neutralizing enemy targets like tanks, functioning as kamikazes (suicide bombs) in a highly cost-effective and powerful strategy. Ukrainian fundraiser United24 recently showcased images of the first 800 out of 3,000 locally built FPV drones being sent to the front lines.

Ukraine’s Ministry of Defense is building a robust drone fleet to enhance its Armed Forces, with UAVs playing a key role in reconnaissance and targeted strikes. In 2024, the Ministry contracted over 1.6M drones worth $2.8B. These include a mix of kamikaze drones, reconnaissance copters, and strike planes, each fulfilling specific operational needs. Looking ahead to 2025, Ukraine plans to contract an additional 155,205 drones worth $0.8B, further boosting its capabilities. The total contracts for 2024 and 2025 will reach nearly $3.5B, highlighting Ukraine’s significant investment in UAV technology.

Modernizing Legacy Systems: The Air Force’s “System 1” Case Study

The US Air Force’s “System 1” plays a crucial role in maintaining aircraft readiness. However, this 20-year-old system runs on COBOL, an outdated programming language, and operates on a mainframe managed by another agency. By 2018, DoD struggled to find personnel skilled in maintaining both the code and its aging infrastructure, with annual upkeep costs reaching $21.8 million.

To address these challenges, the Air Force awarded a contract in late 2018 to migrate “System 1” to the cloud and gradually modernize its COBOL-based code. This shift aimed to improve efficiency, enhance security, and reduce costs—with projected annual savings of $34 million.

This case highlights the broader need for modernizing legacy defense systems. Upgrading outdated infrastructure not only ensures operational reliability but also unlocks long-term cost savings, making the military more agile and prepared for future technological demands.

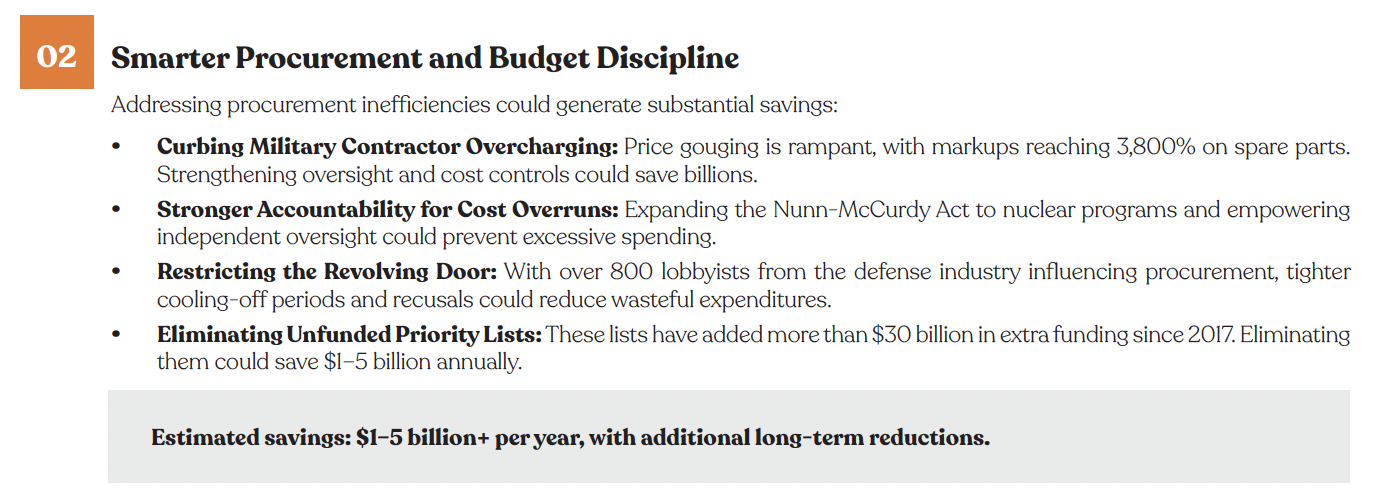

Pushing for a More Efficient, Effective Defense

As the Pentagon’s budget nears $1 trillion annually, inefficiencies and wasteful spending have become a growing concern. In response, organizations such as the Quincy Institute for Responsible Statecraft, Taxpayers for Common Sense, and The Stimson Center have advocated for a leaner, more agile defense strategy with the Department of Government Efficiency to be a facilitator of these reforms.

Four core areas present opportunities for both cost savings and strategic improvement:

Venture capital-backed startups, often at the forefront of cutting-edge technologies like AI, cybersecurity, and autonomous systems, offer a unique opportunity to accelerate defense innovation. The success of companies like SpaceX and Palantir has paved the way for this new wave of defense tech startups, proving that commercial ecosystems can deliver advanced technologies at unprecedented speeds. By strategically engaging with these startups, defense agencies can tap into breakthroughs developed with commercial speed and efficiency.

Benefits of Engaging with VC-Backed Startups

1. Innovation Velocity: Startups, especially those backed by venture capital, are known for their agility and speed in developing innovative technologies. This can help the DoD accelerate the deployment of cutting-edge solutions.

2. Cost Efficiency: Startups often operate with leaner cost structures compared to traditional defense contractors, which can lead to more cost-effective solutions for the DoD.

3. Dual-Use Technologies: Many startups focus on dual-use technologies that can be adapted for military applications, potentially reducing development costs and timelines.

4. Risk Mitigation: Venture capital firms absorb significant early-stage risk, allowing the DoD to invest in proven technologies rather than speculative R&D projects.

5. Talent Acquisition and Retention: Startups can attract and retain top talent in fields like AI, cybersecurity, and quantum computing, which are critical for modern defense capabilities.

VC-Backed Start-ups Need to Align their Innovations with the DoD’s Needs from the Outset

VC-backed start-ups must focus on aligning their innovations with the DoD’s needs from the outset to navigate the complex defense contracting landscape. The DoD has outlined 14 critical technology areas, such as quantum science and AI, which start-ups should target to meet national security priorities. Data shows that only 16% of DoD Small Business Innovation Research (SBIR)-funded companies receive Phase III contracts, and less than 1% of Phase I awardees achieve Program of Record (POR) status. This highlights the “Valley of Death” challenge, where start-ups struggle to move from initial funding to commercialization, underscoring the need for early alignment.

DoD’s Critical Technology Areas and Strategic Priorities

The DoD has identified 14 critical technology areas, such as quantum science, AI, space technology, and advanced computing, as outlined in the National Defense Science and Technology Strategy (NDSTS) in 2023 and the 2022 technology vision. These areas are designed to ensure national security and address emerging threats, making it imperative for start-ups to align their innovations with these priorities from the beginning. For instance, the 2024 Replicator initiative, with a $500 million budget for autonomous drone systems (ADA2), highlights the DoD’s focus on scalable, innovative solutions, where start-ups can play a pivotal role if aligned correctly.

The business aspect here is significant: VC-backed start-ups, with investments like $70 billion deployed in 2022-2023 and 2024 on track for $25 billion, are increasingly targeting these areas to attract DoD contracts [1]. However, misalignment can lead to wasted resources, as start-ups may develop technologies that do not meet DoD specifications, such as security clearances or interoperability standards, which are critical for defense applications.

Low Success Rates and the “Valley of Death”

In the 1960s, DOD drove innovation and was the leading early adopter of new technology sectors. In the first year of that decade, defense-related R&D represented 36% of overall defense expenditure. By 2019, that figure had fallen to just 3%, underscoring that the defense industry has also slowed its pace in research. In 1956, aerospace and defense companies spent 19% of their sales on R&D – several times more than civilian industries – including scientific instruments and chemicals. Today, most defense companies spend just 1-2% of sales on reimbursable R&D, but tech companies spend far more. Last year, Nvidia spent 27% of its sales on R&D, Meta spent 29%, while Amazon devoted $85 billion to technology and infrastructure. DOD cannot spend its way back into technology leadership in most critical technology areas, including AI, communications, advanced materials, microelectronics, space, and cybersecurity. Even hypersonic vehicle development is affected. There are startups – with significant private capital – making these vehicles and trying to use defense as an early sales path to commercial scale.

DOD must leverage the talent, technologies, and capital of the technology sector and integrate them into novel weapon systems concepts. Rapid acquisition procedures can work for small drones and the largest weapon systems alike. This is not a novel observation. More than 30 years ago, the Packard Commission recognized that the technology sector was three to five years ahead of defense. The Federal Acquisition Streamlining Act of 1994 and the Federal Acquisition Reform Act of 1996 created commercial item procedures and preferences for commercial products and services. This period also saw the expansion of DOD authorities to access more nontraditional defense contractors by using Other Transactions – a special type of contract that bypasses contract regulations to facilitate research and prototyping. However, the foundation of commercial items did not stick, and it slowly fell away. The number of government-unique clauses in a commercial contract has increased from roughly 50 to over 150. Even making minor customization for defense is not a minor inconvenience. It imposes hundreds of burdensome clauses and processes on commercial companies.

Integration of defense tech startups is improving, with a notable shift in the sector after a period of decline in investment following the Cold War. During that time, the internet and software industries surged, becoming the dominant wealth generators in VC. As VC interest in defense waned, the US defense industry became increasingly consolidated, with a few major firms now controlling the majority of federal contract procurement. However, recent international conflicts have sparked renewed private investment in national security, revitalizing interest in defense technologies.

In 2023, the US DOD released the National Defense Science and Technology Strategy (NDSTS), highlighting the need to leverage critical emerging technologies to enhance national security. This follows the 2022 technology vision by Undersecretary Heidi Shyu, which identified 14 key technology areas, including quantum science, AI, autonomy, and space technologies, among others, for enhanced defense. To further this objective, the DOD has launched several innovation initiatives to accelerate the development and deployment of new technologies in collaboration with startups. Key organizations within these initiatives include the Defense Innovation Unit (DIU), which scales defense innovation through private sector collaboration; the Office of Strategic Capital (OSC), which attracts and scales private investment to strengthen national security; and the National Security Innovation Capital (NSIC), which funds hardware startups focused on defense challenges. Additionally, AFWERX, the Air Force’s innovation arm, connects with the startup ecosystem, while NavalX facilitates collaboration between the Navy, private companies, academia, and federal agencies. The Army Applications Lab plays a crucial role in bridging funding and testing gaps for new technologies.

DoD Initiatives to Foster Alignment

The DoD has established several initiatives to bridge the gap between innovation and production, encouraging start-ups to align with its needs. The Defense Innovation Unit (DIU), with a 2024 budget of $983 million (up from $70 million in 2023), focuses on adopting commercial technology through OTAs, which are faster and more flexible than traditional contracts. Other organizations, such as the Office of Strategic Capital (OSC), National Security Innovation Capital (NSIC), AFWERX, NAVALX, and the Army Applications Lab, also aim to connect start-ups with DoD needs, providing funding and mentorship.

For instance, DIU’s increased budget reflects a strategic shift toward integrating start-up innovations, but start-ups must align their technologies with DoD priorities to access these resources. This alignment is crucial for navigating the complex procurement process, as seen with the DIU’s focus on critical areas like cybersecurity and autonomous systems, where start-ups like Reality Defender and Shield AI have found success by targeting these needs early.

About Manhattan Venture Partners

Our Research Methodology

Manhattan Venture Research provides clients with accurate, timely, and innovative research into the companies and sectors we cover. To that end, we have established an experienced team of analysts, researchers, economists, and industry veterans that focus exclusively on private companies with a proven track record of success. Producing quality research on a private company is uniquely challenging. Our analysts communicate with ex-employees, early investors, VCs, competitors, suppliers, and others to gather valuable information about the company under coverage. This information enables us to create unique financial models that value the underlying company and provide insight to our clients and industry experts, leveraging years of experience working for bulge bracket firms. Manhattan Venture Research reports include business and financial aspects of late-stage companies. These reports include but are not limited to industry overviews, competitor analysis, SWOT analysis, products (existing and in development), management and key directors, risks and concerns, other proprietary channels, historical financials, revenue projections, valuations (using various matrices and valuation recommendation), waterfall analysis, and a capitalization table.

Information Access Level Classification System (IALCS)

Manhattan Venture Research uses an Information Access Level Classification System (IALCS) to make clear the degree of access offered by the company(s) covered in all research reports.

Each research report is classified into one of three categories depending on its classification. The categories are:

I++: The company covered by the research report provided substantial disclosures to Manhattan Venture Partners.

I+: The report was prepared following partial disclosure by the company, including publicly available financial statements, and/or is based on conversations with past or present company employees.

I: All reports are prepared using a mosaic research approach. Not all companies are willing and able to provide substantive access to management and information. In I reports no direct access was granted.

About the Analyst

Santosh Rao has over 25 years of experience in equity research with a primary focus on the technology and telecom sectors. He started his equity research career at Prudential Securities and later moved to Dresdner Kleinwort Wasserstein, Gleacher & Co, and Evercore Partners, where he followed Telecom and Data Services. Prior to joining Manhattan Venture Partners, he was the Managing Director and Head of Research at Greencrest Capital, focusing on private market TMT research. Santosh has an undergraduate degree in Accounting and Economics, and an MBA in Finance from Rutgers Graduate Business School. While at Gleacher & Co he was ranked leading telecom equipment analyst by Starmine/Financial Times

DISCLAIMER

I, Santosh Rao, certify that the views expressed in this report accurately reflect my personal views about the subject, securities, instruments, or issuers, and that no part of my compensation was, is, or will be directly or indirectly related to the specific views or recommendations contained herein.

Manhattan Venture Research is a wholly-owned subsidiary of Manhattan Venture Holdings LLC (“MVP”). MVP may currently and/or seek to do business with companies covered in its research report. Investors should consider this report as only a single factor in making their investment decision. This document does not contain all the information needed to make an investment decision, including but not limited to, the risks and costs.

Additional information is available upon request. Information has been obtained from sources believed to be reliable but Manhattan Venture Research or its affiliates and/or subsidiaries do not warrant its completeness or accuracy. All pricing information for the securities discussed is derived from public information, unless otherwise stated. Opinion sand estimates constitute our judgment as of the date of this material and are subject to change without notice. Past performance is not indicative of future results. MVP does not engage in any proprietary trading or act as a market maker for securities. The user is responsible for verifying the accuracy of the data received. This material is not intended as an offer or solicitation for the purchase or sale of any financial instrument. The opinions and recommendations here in do not consider individual client circumstances, objectives, or needs and are not intended as recommendations of particular securities, financial instruments, or strategies to particular clients. The recipient of this report must make its own independent decisions regarding any securities or financial instruments mentioned herein. Periodic updates maybe provided on companies/industries based on company-specific developments or announcements, market conditions, or any other publicly available information.

Copyright 2025 Manhattan Venture Research LLC. All rights reserved. This report or any portion hereof may not be reprinted, sold, or redistributed, in whole or in part, without the written consent of Manhattan VentureResearch. Research is offered through VNTR Securities LLC.

Download the report below to read more

What’s a Rich Text element?

Heading 3

Heading 4

Heading 5

The rich text element allows you to create and format headings, paragraphs, blockquotes, images, and video all in one place instead of having to add and format them individually. Just double-click and easily create content.

Static and dynamic content editing

A rich text element can be used with static or dynamic content. For static content, just drop it into any page and begin editing. For dynamic content, add a rich text field to any collection and then connect a rich text element to that field in the settings panel. Voila!

How to customize formatting for each rich text

Headings, paragraphs, blockquotes, figures, images, and figure captions can all be styled after a class is added to the rich text element using the "When inside of" nested selector system.