Venture Bytes #98: Vertical Robotics Presents a Compelling Investment Opportunity

Vertical Robotics Presents a Compelling Investment Opportunity

In the last five years, robotics has become an important part of the venture landscape globally with $90 billion invested between 2018 and 2022, per data from Pitchbook. Vertical robotics, a subsegment of robotics, focused on building vertical-specific robotics across industries including logistics, medical, defense and security, manufacturing, agriculture, construction, and mining, has been the primary driver of VC investment in robotics. With more companies becoming receptive to deploying automation at scale, the addressable market in these industries continues to expand.

Robotics has always been a challenging sector for investors due to its capital-intensive and deep-tech nature. However, the pandemic and the resultant labor shortage and high labor cost brought in a significant shift in this sector as companies started seeking out robotic solutions. In a testament to this shift, a record 517,385 new industrial robots were installed in 2021 globally, up 31% year-on-year, and 32% from the pre-pandemic year of 2019, per World Robotics. The trend continued in 2022 also with a record 44,196 robot units sold in North America, up 11% year-on-year, per data from the Association for Advancing Automation.

This mainstream integration of robotics into investment portfolios is due to various factors, with technological advancements taking the lead. Improvements in technology such as sensing, LIDAR, and increased power have helped robotics adoption by businesses. Accordingly, robot performance has improved 33 times since 2015, per data from ARK Investment Management.

Cost is another important factor behind the VCs’ enthusiasm for robotics investment. The average cost of industrial robots fell from over $68,000 in 2005 to $27,000 in 2017, with a further decline expected to $10,800 in 2025, per Statista. The cost-effectiveness, combined with the rising labor cost and advancements in AI, processing power, machine vision, sensors, and other technologies, has prompted companies to embrace robotics, catalyzing their integration into various operational domains.

While robotics adoption is seeing an uptick, there remains a massive addressable market. Warehouses and fulfillment centers, despite being the most saturated space in robotics, offer tremendous room for growth for robotics adoption. Currently, over 80% of warehouses lack automation in the US, per Makreo Research and Consulting. Additionally, keeping up with the demand for warehouse workers has been difficult. The logistics industry has added 612,000 jobs since 2020 with an average salary for warehouse workers currently at $23 per hour. Additionally, warehouse turnover rates are a whopping 43% and the cost to replace a warehouse worker currently stands at $8,500, per data from the Bureau of Labor Statistics and Kane Logistics. The increasing cost pressure makes warehouses an ideal candidate for robotics adoption. California-based Dexterity is one of the few robotics start-ups offering robots-as-a-service (RaaS) solutions to automate pick and place tasks in warehouses, logistics, and supply chains. Founded in 2017, the company raised a Series B round in October 2021, valuing it at $1.4 billion. Georgia-based GreyOrange, which raised a Series D funding round in May 2022, unifies AI-driven software and mobile robotics to modernize order fulfillment and optimize warehouse operations in real time, leading to speed, agility, and precision in the operations.

Healthcare is another prominent area ripe for robotics adoption. With the baby-boomer cohort in ‘caregiving age’ likely to more than double in the next 10 years, humans won’t be able to fill the gap and robots are likely to play a critical role. Further, 97% of US hospitals are facing nursing shortage, per McKinsey. Hospitals can program robots to distribute medicines and reach any floor and return to the hospital pharmacy for refilling. Texas-based Diligent Robotics is filling the gap with autonomous hospital service robots to support and empower the patient care team. Cedars-Sinai Medical Center introduced Diligent’s flagship robot Moxi in neurology, orthopedic, and surgery units, which saved clinical teams nearly 300 miles of walking within six weeks of the initial implementation.

Industries like construction, manufacturing and agriculture are also ripe for automation. The climate change mitigation pressure is forcing these areas to modernize their processes in new ways that include robotics. Robots with pneumatic arms can be used for automatic crop harvesting. Similarly, start-ups like Texas-based Icon, and San Francisco-based Built Robotics and Canvas Construction are likely to play a key role in mainstream adoption of robotics in construction. In manufacturing, a significant shortfall of around 2.5 million workers is projected in the US to match the demands of normal economic growth. This burgeoning gap underscores the necessity for automation within this sphere. According to ARK Investment Management, Amazon has 3,200 robots for every 10,000 employees, a stark contrast to a mere 140 in the manufacturing industry. To match Amazon’s robot density, the US manufacturing sector would need around four million robots, approximately six times the current global industrial robot sales.

In addition, generalist robots are shaping up to be the next big robotics success stories. With the growth of multimodal AI models, we see a huge opportunity for robotics to become multipurpose because these models enable common sense and require little training. In March, Google unveiled its multimodal embodied visual-language model (VLM) PaLM-E, a generalist robot brain that takes commands. The VLM is trained on 562 billion parameters that integrate vision and language for robotic control.

With potential applications across industries, the robotics sector remains exciting with a bright future of exponential growth ahead. Analysts foresee the need for 10x more robotics startups to meet the future demand. The ongoing surge in interest and investment marks a significant testament to both the adaptability of businesses and the maturation of robotic technologies.

AI Driving Carbon Capture and Storage Efficiency

In the ever-evolving landscape of innovation, two themes currently stand out prominently – the meteoric rise of artificial intelligence (AI) startups and the pressing need for efficient carbon capture and storage (CCS) solutions. The convergence of these two domains presents a paradigm-shifting opportunity in the climate tech sector.

The US Energy Department recently announced $1.2 billion to build two commercial-scale direct air capture facilities in Texas and Louisiana. President Joe Biden’s Bipartisan Infrastructure Law is funding the initiative which is part of the Regional Direct Air Capture Hubs program. Despite huge government spending in this area, traditional methods often lag in efficiency, struggling to match the urgency that the climate crisis demands.

Accordingly, new-age start-ups integrating AI with carbon capture and storage promise to solve these inefficiencies. VCs realize the opportunity these start-ups, part of the broader climate software sector, offer and are investing heavily in them. Broadly, carbon tech start-ups pulled in $13.8 billion in VC deals in 2022 across sectors including carbon fintech and consumer, biological carbon removal, direct air capture, point-source carbon capture, carbon accounting and analytics, and carbon utilization.

AI’s ability to predict and refine outcomes is the game-changing factor that can overhaul the CCS process. For instance, cutting-edge image processing algorithms help identify carbon emissions in industrial settings. AI models utilizing satellite data help monitor and analyze emissions on a global scale. AI, combined with natural language processing, allows the prediction of optimal materials for carbon separation. These predictive capabilities enable businesses and governments to forecast emissions and set reduction targets effectively.

One of the most common methods for carbon capture and storage is point-source carbon capture, which involves capturing carbon dioxide at its point of emission from industrial plants. Notably, Nvidia’s AI technology, leveraging the fourier neural operators architecture, can lead to an impressive 700,000-fold acceleration in carbon capture and storage modeling. This advancement dramatically enhances the speed of carbon sequestration simulations from years to mere seconds, marking a significant leap forward in environmental impact assessment.

The startups offering AI and ML-powered solutions for carbon capture and storage will benefit from the overall growth of the total addressable market. The global carbon capture, utilization, transportation, and storage market was valued at $3 billion in 2022 and is projected to reach $14.2 billion by 2030 at a CAGR of 21.5%, per MarketsandMarkets.

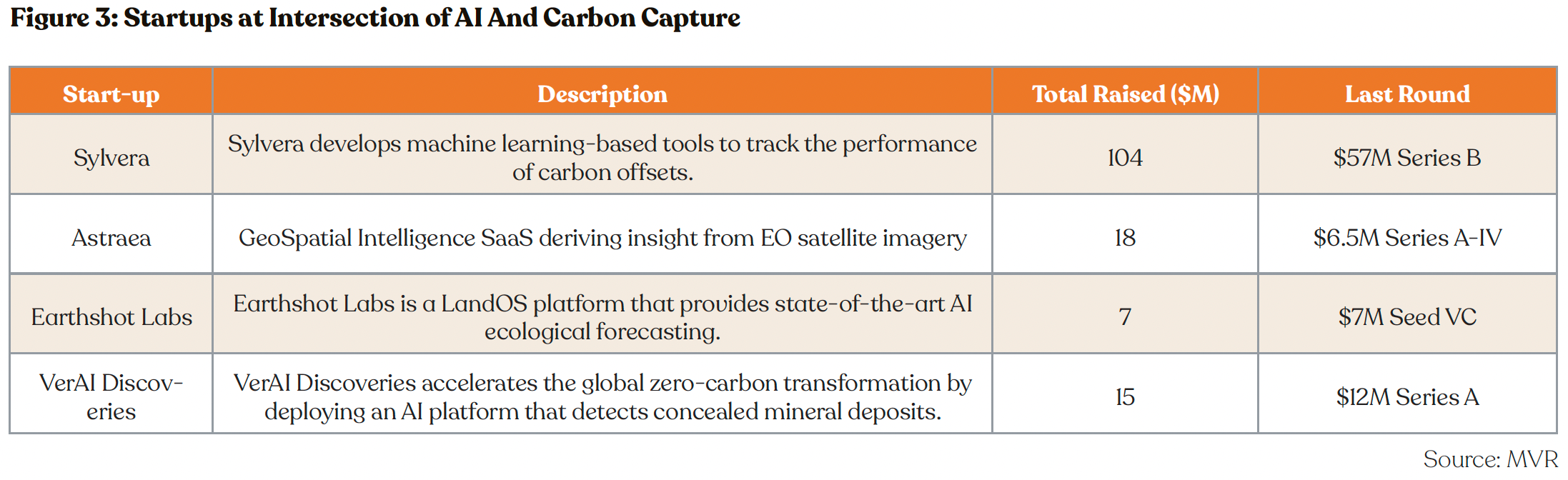

San Francisco-based Pachama, which uses satellite data and AI software to help companies vet and invest in carbon credits, raised its $55 million Series B round in 2022. BluWave-ai, another prominent start-up leveraging AI to improve carbon capture, balances the cost, availability, and carbon footprint of different energy sources and energy storage, along with demand, in real time. This smart use of AI in decision-making marks a significant step forward in our journey toward a greener future. UK-based Sylvera has secured $104 million in total funding, with its machine learning-based tools effectively monitoring carbon offsets’ performance. Virginia-based Astraea excels in GeoSpatial Intelligence, harnessing insights from EO satellite imagery. The innovative approaches of these start-ups to carbon capture efficiency align perfectly with the growing demand for sustainable practices, offering them a strategic edge in a competitive landscape.

Moreover, incorporating technologies like AI in the broader corporate sustainability sector offers incentives for businesses as well. Research from Boston Consulting Group suggests a profound opportunity at the intersection of AI and corporate sustainability. Leveraging AI has the potential to contribute significantly to the required reduction in emissions, targeting 5% to 10% of the total, translating to a range of 2.6 to 5.3 gigatons of CO2 equivalent. The research findings also suggested a substantial economic upside, where the application of AI to corporate sustainability could yield an overall value between $1.3 trillion to $2.6 trillion by 2030.

Furthermore, artificial intelligence has become a game changer when it comes to estimating carbon storage capacity volume using sparse 2D/3D seismic data. To achieve realistic estimates of carbon storage capacity, various sources of relevant past data are integrated and ingested. This data is then subjected to analysis, pre-processing, and data engineering, enabling the computation of the Relative Storage Index (RSI). RSI is an ML-predicted value that can be used to define suitable storage ranges for different geological areas. This helps provide a better understanding of the strengths and weaknesses of subsurface storage.

Artificial Intelligence has significantly enhanced the creation of data-centric geological models for forecasting subsurface carbon dioxide storage capacity. Recent use cases demonstrate that data-driven machine learning solutions can expedite carbon capture by as much as tenfold compared to traditional modeling methods, offering a streamlined workflow. This amalgamation of current and past location data simplifies decision-making, leading to diminished environmental risks.

What’s a Rich Text element?

Heading 3

Heading 4

Heading 5

The rich text element allows you to create and format headings, paragraphs, blockquotes, images, and video all in one place instead of having to add and format them individually. Just double-click and easily create content.

Static and dynamic content editing

A rich text element can be used with static or dynamic content. For static content, just drop it into any page and begin editing. For dynamic content, add a rich text field to any collection and then connect a rich text element to that field in the settings panel. Voila!

How to customize formatting for each rich text

Headings, paragraphs, blockquotes, figures, images, and figure captions can all be styled after a class is added to the rich text element using the "When inside of" nested selector system.