True Anomaly: Pure-Play Autonomous Space Defense Platform

Summary

The previous era of the space economy was defined by lowering the cost of reaching space orbit. The next era will be defined by controlling, coordinating, and defending orbital infrastructure. In that transition, launch providers alone may not capture the greatest long-term strategic value. Instead, the most defensible position will belong to companies building the operational layer for contested space environments. True Anomaly is positioning itself within that operational layer, a mission-critical layer focused on autonomous space defense, orbital maneuverability, and space-to-space operations. The company develops purpose-built orbital vehicles and software designed to operate at significantly lower cost and with greater flexibility than legacy systems. The company is well positioned to benefit from the rapid growth in orbital activity, increasing demand for space security and maneuverability, and the expansion of strategic infrastructure in orbit. True Anomaly has demonstrated strong product-market fit through successful mission execution, major government contract wins, and participation in high-priority US defense programs. Led by an experienced team with deep expertise in defense and aerospace, the company is positioned to capitalize on long-term national security trends. True Anomaly was last valued at $2.2B in April 2026, with projected revenue growth from $64M–$116M in 2026 to $289M–$396M by 2031, per Manhattan Venture Research (MVR).

Methodology

Our views on True Anomaly are derived from our rigorous research process, involving proprietary channel checks with users, competitors, and industry experts, and synthesizing publicly available information from the company and other reliable sources.

Key Points

Purpose-Built for Space-to-Space Operations: Unlike legacy space defense assets designed primarily to support ground operations, True Anomaly’s autonomous orbital vehicles (AOVs) and software stack are purpose-built for space-to-space missions, delivering industry-leading maneuverability at a fraction of the cost of legacy systems.

Scaling with the Growing Need for Rendezvous and Proximity Operations (RPO): Since 2020, the number of objects in orbit has grown at an unprecedented rate, increasing the need for advanced satellite maneuvering, space traffic management, and orbital security capabilities. In 2025 alone, global space activity reached record highs, with more than 300 successful launches and approximately 4,500 payloads deployed into orbit. Against this backdrop, True Anomaly is emerging as a critical player in the next generation of space security and autonomous orbital operations.

Rapidly Expanding End-Use Market: Over the next decade, strategic infrastructure in orbit is expected to expand significantly across energy generation, compute infrastructure, and missile defense systems. As governments and commercial operators deploy increasingly high-value space assets, demand will grow for autonomous spacecraft capable of security, maneuverability, inspection, coordination, and tactically responsive operations. True Anomaly is well positioned to capitalize on these long-term secular trends through its focus on AOVs, software-defined space operations, and mission architectures aligned with evolving national security priorities.

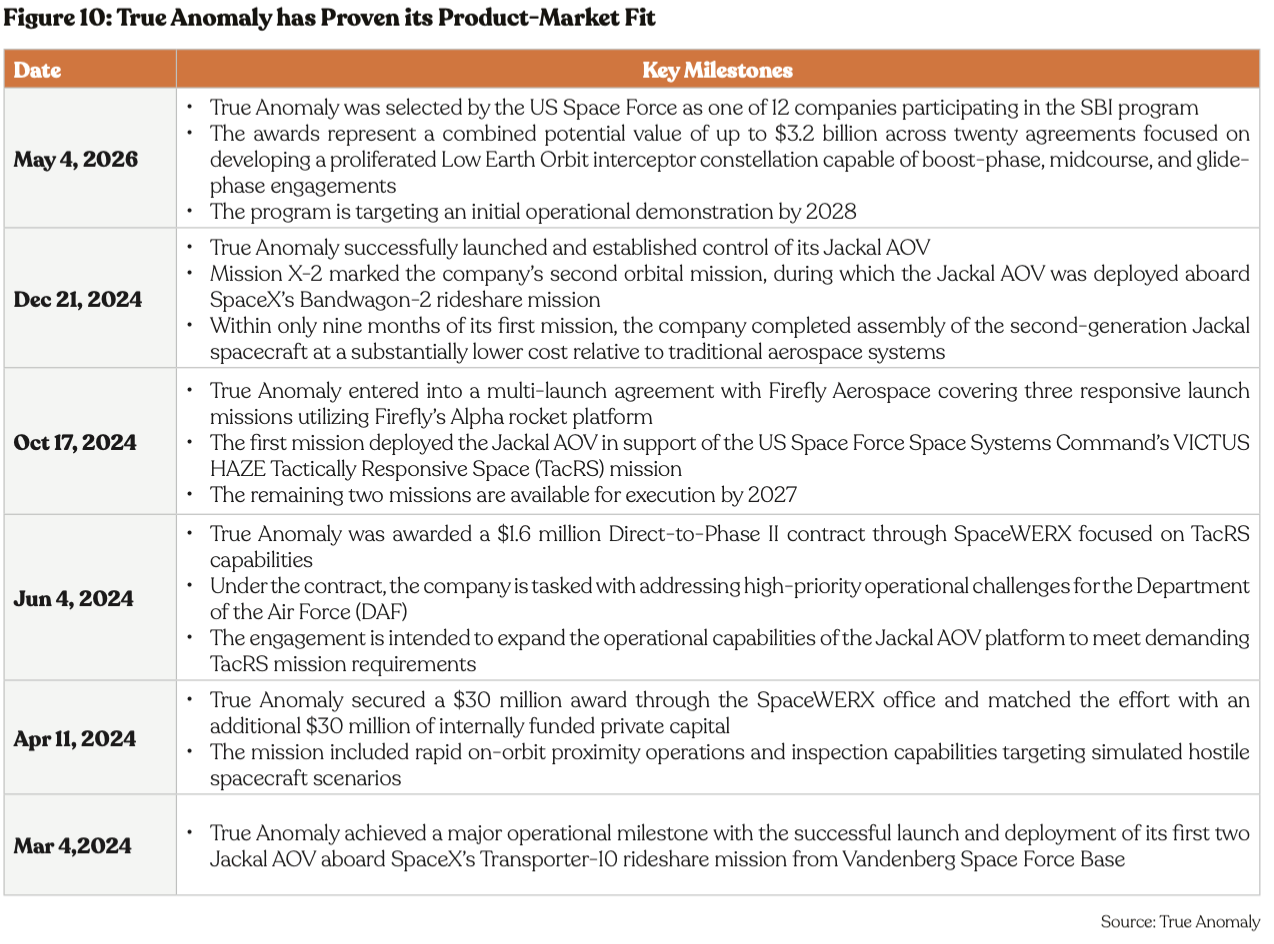

Strong Product-Market Fit: True Anomaly has demonstrated strong product-market fit through consistent mission execution, strategic government contract awards, and growing operational relevance within the US national security space ecosystem. Between 2024 and 2026, the company advanced from launching and validating its first AOVs to participating in multi-billion-dollar defense initiatives and tactically responsive space programs, underscoring both its technical credibility and increasing institutional demand for autonomous space defense capabilities.

Experienced Leadership Team: Backed by a leadership team with deep expertise in defense technology and space operations, True Anomaly is well positioned at the forefront of the space and defense sector. Co-founders Even Rogers and Kyle Zakrzewski bring extensive operational, engineering, and strategic experience across military space systems, aerospace engineering, and national defense technologies.

Key Challenges: Dependence on Government Procurement Cycles & Budget Priorities and Intensifying Competitive Landscape: True Anomaly faces exposure to government procurement cycles and evolving budget priorities, as defense contracting involves complex, multi-year processes shaped by changing requirements, political oversight, funding negotiations, and shifting strategic objectives. The company also operates within an increasingly competitive landscape, facing established incumbents such as SpaceX and Lockheed Martin, among others.

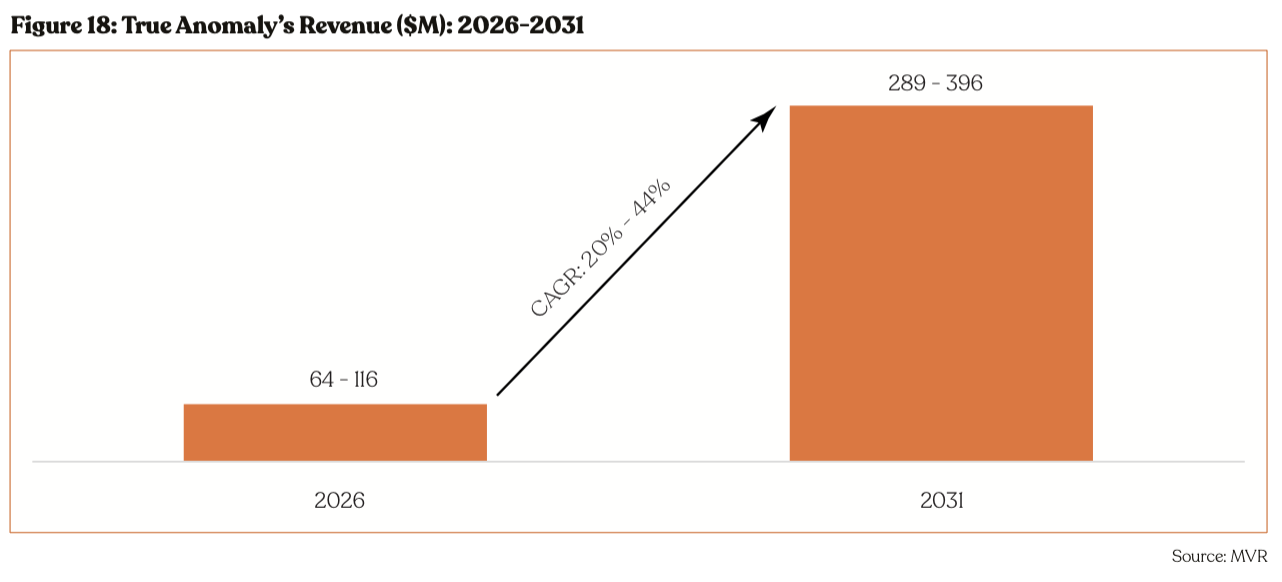

Valuation: True Anomaly’s last reported private valuation was $2.2B as of April 2026. MVR projects True Anomaly’s 2026 revenue between $64M and $116M, with a trajectory toward $289M - $396M by 2031.

Executive Summary

True Anomaly is purpose-built for space-to-space operations, offering AOVs and a software-defined stack that delivers superior maneuverability at lower cost than legacy systems. Rapid orbital congestion and record launch activity are driving urgent demand for RPO, space traffic management, and orbital security, positioning True Anomaly as a critical provider for next-generation space defense and autonomous operations. The firm’s product-market fit is validated by repeated mission successes, strategic government contract awards, and escalated participation in multi-billion-dollar defense programs. With secular growth expected in orbital energy, compute, and missile-defense infrastructure over the coming decade, True Anomaly’s focus on autonomous spacecraft, software-first mission architectures, and alignment with national security priorities creates a clear commercial pathway. The company benefits from experienced leadership (co-founders Even Rogers and Kyle Zakrzewski) but remains exposed to government procurement cycles, shifting budget priorities, and competition from incumbents. Last reported private valuation was $2.2B (April 2026); MVR projects 2026 revenue of $64M–$116M, rising toward $289M–$396M by 2031.

Why Now?

With space poised to become the next frontier for compute (space-based data centers), energy (space solar power), and defense (orbital missile interception), True Anomaly represents a compelling investment. Its AOVs and end-to-end software stack are strategically positioned to capture growing demand for space defense infrastructure across these expanding markets.

Company Overview

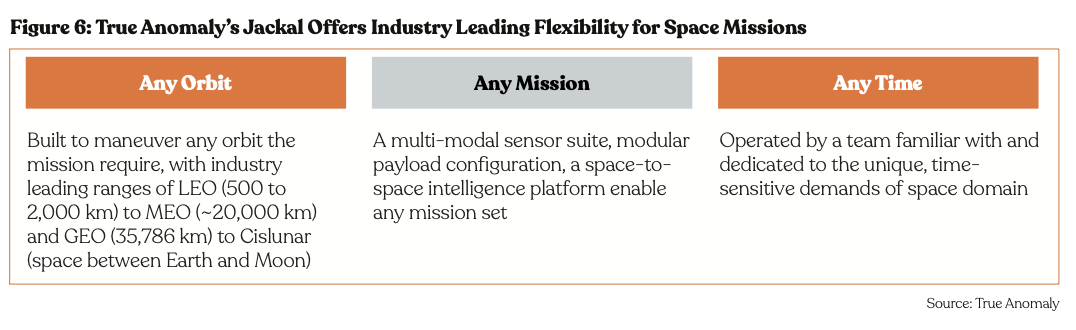

True Anomaly’s core product portfolio consists of the Jackal family of highly maneuverable satellites, referred to as AOVs, and the Mosaic software platform that powers them. Together, these systems are designed to advance US space superiority by enabling the United States Department of Defense (US DoD) to protect critical space assets while disrupting adversarial space operations.

Jackal

Jackal is a highly maneuverable satellite platform designed for inter-satellite missions and RPO. Roughly the size of a small refrigerator, the spacecraft functions as a mission-configurable payload platform capable of supporting multiple operational payloads aligned with the United States Space Force mission of achieving and maintaining space superiority.

Jackal satellites are manufactured at True Anomaly’s GravityWorks production facilities. The company’s primary facility is co-located with headquarters in Centennial, Colorado, while a significantly larger GravityWorks site in Long Beach, California, was announced in early 2025 to support scalable, high-volume production of Jackal and future spacecraft systems.

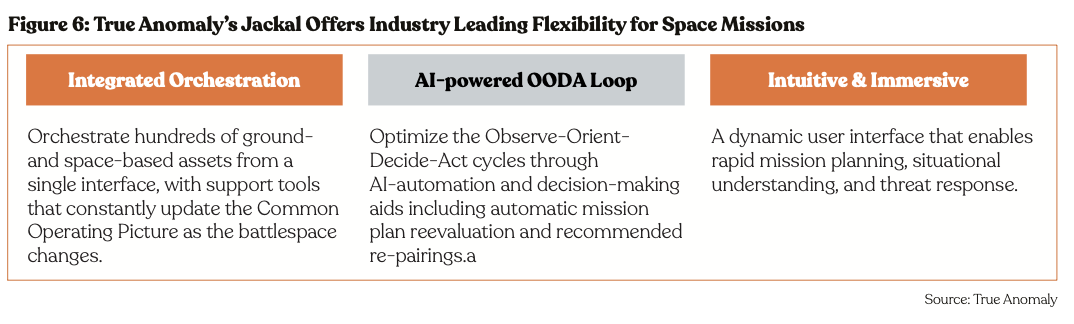

Mosaic

Mosaic is True Anomaly’s full-stack software platform designed to support Jackal and future AOV systems while enhancing space domain awareness for military operators. The platform integrates satellite command and control, mission simulation, autonomous operations, AI-enabled decision support, and operator training capabilities into a unified software environment.

Built using the Elixir programming language for scalability, low latency, and fault tolerance, Mosaic is intended to support resilient real-time space operations. In April 2023, True Anomaly announced a partnership with Viasat and Microsoft Azure to integrate satellite management data from Viasat’s global ground-station network into the Mosaic ecosystem.

Mosaic’s battle management tools are designed primarily for Space Force satellite operators, including Space Operations Officers and Space Systems Operators. The platform aggregates data from both ground-based and orbital sensors to provide enhanced situational awareness through integrated visualization, mission planning, and AI-assisted tactical decision-making tools intended to reduce operator workload and improve operational responsiveness.

The platform also includes a digital range simulation environment that enables virtual testing of complex inter-satellite engagements and RPO missions. This capability supports faster and more effective ground testing while improving mission readiness and operational reliability. The digital range can simulate both friendly and adversarial spacecraft interactions for mission validation and tactical development.

In addition, Mosaic includes the Ascension training environment, a multiplayer command-and-control simulation platform designed to train Space Force Guardians. The system is intended to improve operator readiness, reduce training timelines, and facilitate seamless transition from simulation to live operations through a consistent operational interface.

Beyond simulation and battle management, Mosaic can directly manage AOV operations through human-machine teaming workflows. The platform automates many onboard spacecraft functions while maintaining human supervisory control, reducing operator burden during active missions. Mosaic also operates onboard Jackal spacecraft, enabling onboard sensor integration, autonomous response execution, and efficient transmission of mission data to ground operators.

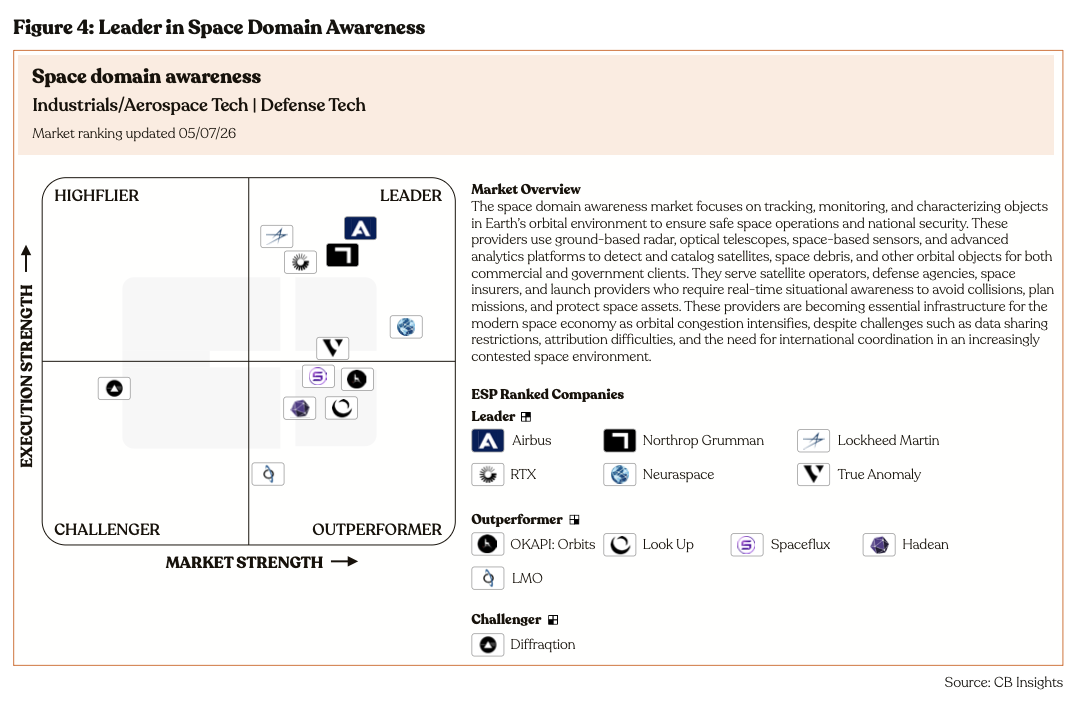

Competitive Benchmarks

True Anomaly has rapidly emerged as one of the leading players in the space domain awareness and orbital defense market, despite being founded only in 2022. The company’s $2.2 billion valuation already approaches the scale of more established peers such as Astranis, highlighting strong investor confidence in the strategic importance of space security infrastructure. While SpaceX remains the dominant benchmark in terms of launch capability, funding, and scale, True Anomaly differentiates itself through its defense-first focus on autonomous orbital warfare and space superiority. Unlike launch providers or satellite operators, the company is building an integrated stack combining spacecraft, AI-driven autonomy, and real-time space domain awareness software designed specifically for contested orbital environments.

Compared with peers such as Orbit Fab and HEO, which focus on narrow infrastructure layers like refueling or observation, True Anomaly is positioning itself as a full-stack orbital defense platform. Its moat lies in the convergence of autonomous spacecraft operations, defense-oriented AI software, and deep integration with US national security priorities. The company’s software-centric architecture could create significant switching costs and data advantages over time, particularly as orbital traffic, satellite threats, and military dependence on space assets continue to increase.

Traditional aerospace businesses are often hardware-heavy with low iteration speed and long deployment cycles. True Anomaly’s software-defined architecture introduces the possibility of recurring software revenue, mission upgrades, fleet coordination systems, autonomy modules, and simulation environments layered on top of spacecraft hardware. Over time, software could become the higher-margin value driver, similar to how Palantir evolved from services into a sticky operational software platform for defense agencies.

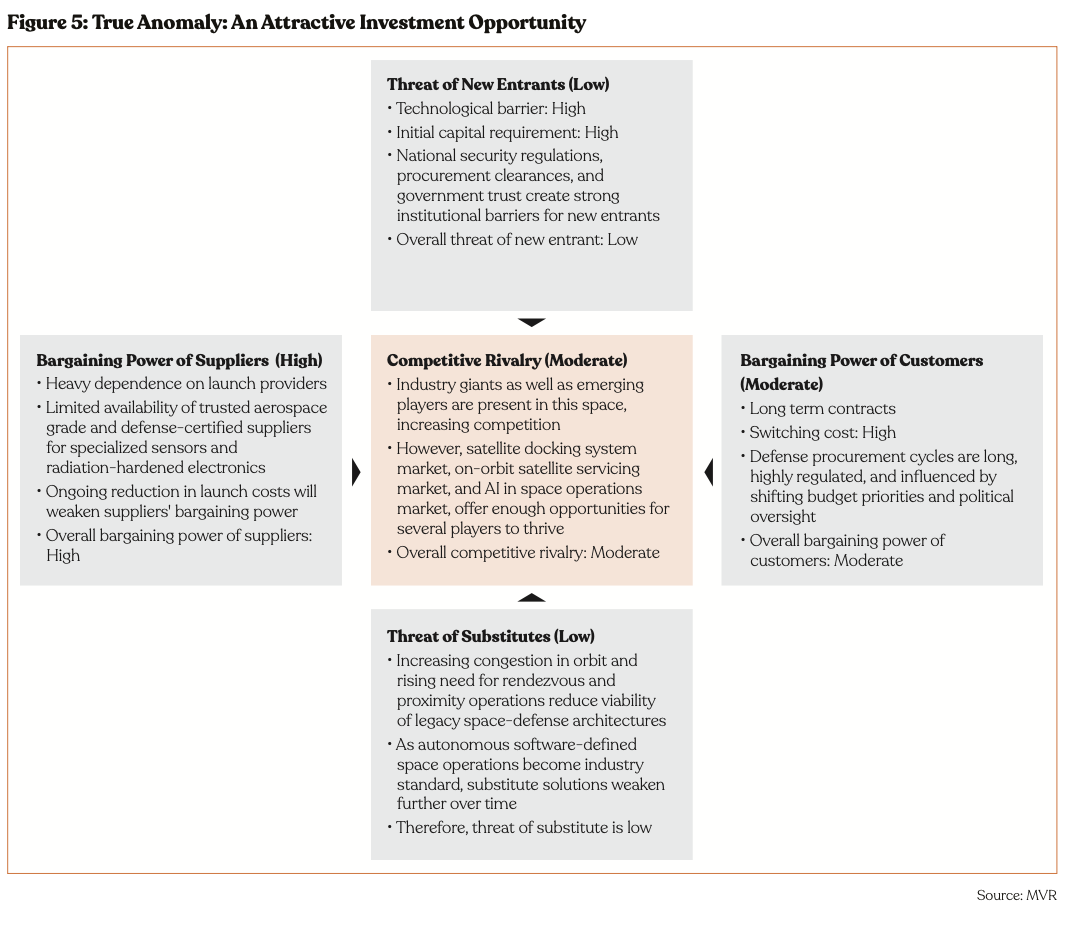

True Anomaly – Strong Competitive Position

True Anomaly is well-positioned within the contested space domain, where autonomous RPO, and space domain awareness are becoming mission‑critical capabilities. Technological complexity, substantial upfront capital needs, and stringent national security regulations create formidable barriers for new entrants, even as large primes and emerging space players intensify competitive rivalry. At the same time, True Anomaly operates in a supply chain still heavily dependent on a limited pool of launch providers and aerospace‑grade, defense‑certified component vendors, resulting in elevated supplier power despite gradually declining launch costs. On the demand side, long defense procurement cycles, high switching costs, and multi‑year contracts temper customers’ willingness and ability to rapidly change vendors, keeping customer bargaining power in a moderate range. Finally, the scarcity of credible substitute architectures for software‑defined, on‑orbit space defense solutions suggests a structurally attractive niche, with substitutes posing a relatively low threat in the medium term.

Key Investment Positives

Purpose-Built for Space-to-Space Operations

Unlike legacy space-based defense assets that primarily support ground operations, True Anomaly develops spacecraft and software

purpose-built for space superiority. Its autonomous satellite, Jackal, is engineered for space-to-space operations, including targeting

adversary satellites and protecting existing US Space Force constellations.

As an alternative to expensive, non-maneuverable or limited-maneuverability satellites, True Anomaly provides cost-effective, highly

maneuverable satellites optimized for inter-satellite operations, such as:

• Space Domain Awareness: tracking and identifying satellites or objects in orbit

• Intelligence, Surveillance, and Reconnaissance (ISR): collecting imagery, signals, or behavioral data from space assets

• Space Security / Defense Operations: monitoring potentially hostile spacecraft activity

• Electronic Warfare Missions: detecting, jamming, or analyzing signals

• Satellite Inspection / Rendezvous Operations: approaching and observing another spacecraft

• Communications Relay: passing data between satellites or ground stations

• Target Characterization: determining what another satellite is doing or carrying

• Autonomous Orbital Operations: coordinated spacecraft maneuvers and monitoring

True Anomaly is not competing in a discretionary commercial market, it is positioning itself within a rapidly expanding national security priority area. As warfare increasingly extends into orbit, governments are likely to treat space domain awareness and orbital maneuverability as strategic necessities rather than optional capabilities. This creates long-duration procurement visibility and reduces the risk of demand evaporation typically seen in commercial aerospace cycles.

Additionally, Mosaic, True Anomaly’s software stack for space operations, reduces operator workload by fusing data from space- and ground-based sensors, links, and on-orbit assets, creating a complete and dynamic Common Operating Picture of the space domain.

Scaling with the Growing Need for RPO

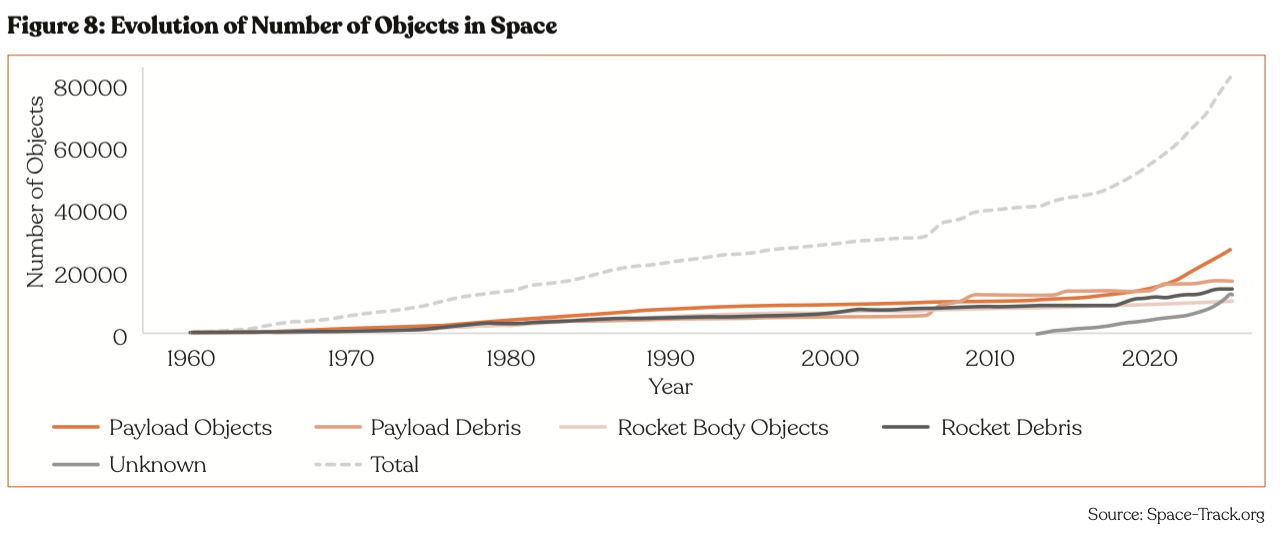

Since 2020, the number of objects in space has expanded at an unprecedented pace, driving a critical need for advanced satellite maneuvering, space traffic management, and orbital security capabilities. In 2025 alone, global space activity reached record levels, with more than 300 successful launches and approximately 4,500 payloads deployed into orbit. Today, Earth’s orbital environment includes roughly 13,000 active satellites alongside an estimated 141 million debris objects.

This rapid increase in orbital density has created a need for executing RPOs. RPOs occur when two spacecrafts or satellites enter the same orbital plane and maneuver in proximity, often enabling inspection, servicing, docking, or other coordinated operations. As these capabilities become more common across both commercial and defense applications, the strategic importance of secure, autonomous, and responsive RPO infrastructure is growing significantly.

The risks associated with an increasingly congested orbital environment are substantial. In a worst-case scenario, operational failures or collisions could accelerate the onset of the Kessler Syndrome, a concept introduced by NASA scientist Donald Kessler in 1978. The theory describes a cascading chain reaction in Low Earth Orbit (LEO), where collisions generate additional debris, triggering further collisions and potentially rendering key orbital regions unusable for decades.

At the same time, geopolitical tensions are reshaping how nations interpret on-orbit behavior. In an environment where every close approach between spacecraft may be perceived as hostile, the lack of transparency and standardized operational norms creates escalating strategic risk. As technological capabilities continue to outpace governance frameworks, the global space ecosystem will increasingly require trusted operators, autonomous coordination systems, and scalable RPO technologies that support both national security objectives and long-term orbital sustainability.

The strategic importance of these capabilities became particularly clear following China’s 2007 anti-satellite (ASAT) test, in which Beijing destroyed one of its aging weather satellites. While China stated the mission was non-hostile, the event intensified global concerns around the militarization of space and the vulnerability of orbital infrastructure.

Against this backdrop, True Anomaly is emerging as a critical player in the next generation of space security and autonomous orbital operations.

In October 2024, United States Space Force selected True Anomaly for the VICTUS HAZE mission, a $60 million tactically responsive space (TacRS) program designed to strengthen the military’s ability to rapidly respond to emerging on-orbit threats. The program includes $30 million in funding from SSC/SpaceWERX through an SBIR award, with True Anomaly contributing an additional $30 million in private capital, a strong signal of both government validation and investor confidence.

The VICTUS HAZE mission will showcase True Anomaly’s Jackal AOV, a platform purpose-built for RPO, autonomous maneuvering, and on-orbit mission execution. In parallel, the company developed the command-and-control infrastructure necessary to enable responsive space operations on a scale.

Data Network Effects from Orbital Operations: Every rendezvous mission, orbital maneuver, anomaly detection event, or satellite interaction generates valuable operational data. As the company executes more missions, its AI systems can improve autonomous navigation, threat detection, and tactical decision-making. This creates a compounding intelligence moat where the company’s software improves through real-world orbital experience, something competitors without active operational fleets may struggle to match.

Rapidly Expanding End-Use Market

The next decade is expected to drive a fundamental expansion of strategic infrastructure in orbit, spanning energy generation, compute infrastructure, and missile defense systems. As governments and commercial operators increasingly deploy high-value assets in space, demand will accelerate for autonomous spacecraft capable of security, maneuverability, inspection, coordination, and tactically responsive operations. True Anomaly is well positioned to benefit from these long-term secular trends due to its focus on AOVs, software-defined space operations, and mission architectures aligned with emerging national security priorities.

Space-Based Solar: The emergence of space-based solar power (SBSP) has the potential to materially expand the addressable market for True Anomaly by creating an entirely new class of high-value orbital infrastructure requiring persistent protection, monitoring, maneuverability, and defense capabilities. Space-based solar systems are expected to consist of large-scale orbital energy generation and transmission assets operating in strategically important orbits for extended durations. These assets would represent critical infrastructure for both civilian energy resilience and national security applications, making them attractive targets for adversarial interference, electronic warfare, proximity operations, and kinetic threats.

As orbital energy infrastructure scales, operators and governments will require autonomous systems capable of space domain awareness, inspection, escort missions, and active deterrence. True Anomaly’s Jackal Autonomous Orbital Vehicle platform is already being positioned within this broader category of orbital security and responsive space operations. The company’s demonstrated ability to execute autonomous rendezvous, maneuvering, and tactical orbital missions positions it as a foundational infrastructure layer for protecting future space-based energy networks. In effect, the growth of SBSP could expand demand for persistent orbital defense platforms in the same way that terrestrial energy infrastructure historically accelerated demand for cybersecurity, physical security, and defense systems.

Additionally, space-based solar architectures are likely to increase the density and economic importance of assets in Low Earth Orbit and adjacent orbital regimes. This drives long-term demand for space traffic management, autonomous coordination, inspection systems, and tactically responsive spacecraft, all areas where True Anomaly is already building operational credibility with the US Space Force. As governments prioritize energy independence and resilient power infrastructure, True Anomaly stands to benefit from both direct defense spending and the broader commercialization of strategic orbital infrastructure.

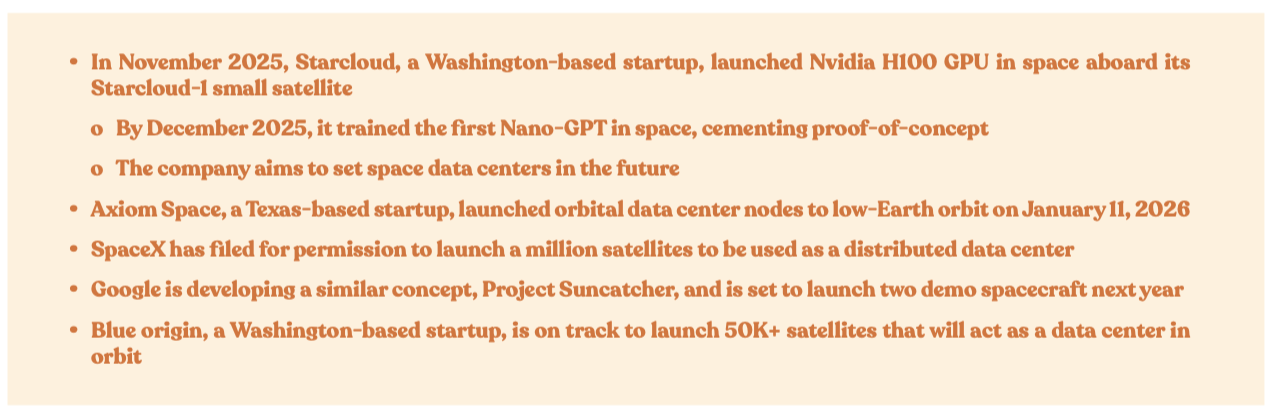

Space-Based Data Centers: The rise of space-based data centers represents another major structural tailwind for True Anomaly. As AI workloads, sovereign compute requirements, and power-constrained terrestrial infrastructure drive interest in orbital compute platforms, space will increasingly evolve from a communications environment into a compute and data infrastructure layer. Space-based data centers are expected to host highly valuable workloads tied to defense, intelligence, AI inference, edge computing, secure communications, and resilient cloud architectures. These assets will require continuous monitoring, servicing, protection, and operational maneuverability.

This trend directly aligns with True Anomaly’s core capabilities. AOVs capable of proximity operations, inspection, threat detection, escort functions, and rapid deployment become significantly more valuable in a future where orbital compute infrastructure carries strategic and economic importance comparable to terrestrial hyperscale data centers. The company’s emphasis on software-defined autonomy and tactically responsive spacecraft creates a differentiated positioning advantage as orbital infrastructure becomes more operationally dense and commercially valuable.

Importantly, the economics of space-based data centers could accelerate demand for lower-cost, rapidly deployable spacecraft architectures. True Anomaly has already demonstrated the ability to iterate and deploy spacecraft on compressed timelines and at costs substantially below legacy aerospace systems. This operational model is particularly attractive in an environment where commercial operators and defense agencies will prioritize scalability, resiliency, and rapid replenishment over bespoke, multi-year satellite procurement cycles.

Space-Based Missile Interception: Space-based missile interception represents one of the most consequential long-term opportunities for True Anomaly and materially increases the company’s strategic importance within the US defense ecosystem. The transition toward proliferated orbital missile defense architectures requires autonomous spacecraft capable of persistent maneuverability, real-time coordination, rapid deployment, and operations in contested environments, capabilities that align closely with True Anomaly’s existing technology roadmap.

The company’s selection by the US Space Force for the Space-Based Interceptors (SBI) program is particularly significant because it validates True Anomaly’s positioning within a next-generation defense architecture that could command tens of billions of dollars in long-duration government spending over the coming decade. Unlike traditional missile defense systems that rely heavily on fixed terrestrial infrastructure, space-based interception architectures require distributed autonomous orbital systems capable of operating dynamically across multiple engagement phases, including boost, midcourse, and glide-phase interception scenarios.

True Anomaly’s Jackal platform and broader autonomy stack are well aligned with this evolving operational doctrine. AOVs capable of maneuvering in contested environments, conducting rapid threat assessment, coordinating with distributed constellations, and executing tactically responsive missions become increasingly critical as the US DoD shifts toward resilient, proliferated space defense networks. The company’s focus on software-driven orbital operations also positions it favorably relative to legacy aerospace contractors that are often constrained by slower procurement cycles and less agile hardware architectures.

From an investment perspective, missile defense also creates unusually durable revenue visibility and strategic alignment with national security priorities. Space-based interception is increasingly viewed as a critical component of future deterrence strategy amid rising geopolitical competition and advancements in hypersonic weapons systems. As a result, companies successfully integrated into this ecosystem are likely to benefit from sustained procurement demand, expanding program scope, and long-term government partnerships. True Anomaly’s early participation in these initiatives substantially increases the probability that the company evolves from a tactical spacecraft provider into a core defense infrastructure platform within the broader national security space economy.

Beneficiary of the Exploding Orbital Economy: The number of satellites and orbital assets is increasing exponentially due to mega-constellations, earth observation, telecom, and defense deployments. As orbit becomes more crowded, demand rises for orbital traffic management, proximity operations, security monitoring, and autonomous maneuvering systems. True Anomaly benefits not only from defense demand, but also from the structural complexity created by orbital congestion itself.

Strong Product-Market Fit

True Anomaly has demonstrated clear product-market fit through a consistent cadence of mission execution, strategic government contract wins, and expanding operational relevance within the US national security space ecosystem. Over a two-year period between 2024 and 2026, the company progressed from launching and validating its first AOVs to securing participation in multi-billion-dollar defense initiatives and tactically responsive space programs. The company’s ability to rapidly iterate hardware, execute missions alongside leading aerospace partners, and secure repeat engagement from the US Space Force highlights both technical credibility and growing institutional demand for its autonomous space defense capabilities.

Experienced Leadership Team

Backed by deep expertise in defense technology and space operations, True Anomaly is positioned at the forefront of the space and defense sector. Co-founders Even Rogers and Kyle Zakrzewski bring extensive operational, engineering, and strategic experience across military space systems, aerospace engineering, and national defense technologies.

Even Rogers, CEO & Co-Founder: Even Rogers is the CEO and co-founder of True Anomaly, where he leads the development of advanced hardware and software solutions focused on space superiority. During the formative years of the US Space Force, he served as an Air Force space operations officer, developing tactics to protect military space assets from emerging threats. His leadership experience spans space systems development and operational testing, training, spacecraft operations, and joint fires coordination. He led multidisciplinary teams of space operators, scientists, and engineers, gaining deep expertise in the vulnerabilities of US space systems and associated technology and intelligence gaps.

Kyle Zakrzewski, Chief Engineer & Co-Founder: Kyle Zakrzewski leads the design, development, and production of True Anomaly’s mission solutions. Prior to co-founding the company, he served as Orbital Warfare Chief of Training for the US Air Force’s 26th Space Aggressor Squadron, where he specialized in advanced space warfare training exercises. His military leadership experience also includes roles as Maintenance Flight Commander and Officer in Charge of Protected SATCOM Operations for the 4th Space Operations Squadron, as well as service as an Air Force Cyberspace Operations Officer. Before joining True Anomaly, Kyle worked as a Guidance, Navigation, and Controls Engineer for National Defense Space Systems at Ball Aerospace and Technologies from 2017 to 2022. He also held systems engineering roles at Lockheed Martin Electronic Systems and Honeywell Aerospace.

Key Investment Concerns

Dependence on Government Procurement Cycles and Budget Priorities

One of the primary investment risks for True Anomaly is the company’s significant dependence on US government procurement programs, particularly within the US DoD and US Space Force ecosystem. While the company has demonstrated strong early traction through SpaceWERX awards, tactically responsive space programs, and participation in next-generation missile defense initiatives, a meaningful portion of its projected long-term revenue opportunity remains tied to government adoption timelines, congressional appropriations, and evolving national security priorities.

Defense procurement cycles are inherently complex, multi-year processes characterized by changing requirements, political oversight, budget negotiations, and shifting strategic priorities. Programs that appear strategically critical today may experience delays, restructuring, reduced funding allocations, or outright cancellation depending on broader macroeconomic conditions or changes in administration priorities. Additionally, many of the large market opportunities associated with SBI, orbital defense infrastructure, and tactically responsive space systems remain in relatively early stages of operational deployment. As a result, there is still uncertainty regarding the speed at which prototype programs translate into scaled production contracts and recurring procurement revenue.

Competitive Pressure from Vertically Integrated Defense and Space Giants

The long-term opportunity areas that support the True Anomaly investment thesis, including tactically responsive space, autonomous orbital operations, missile interception, and space domain awareness, are also strategically important markets for the largest aerospace and defense companies in the world, such as SpaceX, Lockheed Martin, etc.

At the same time, the presence of these incumbents is not entirely negative for True Anomaly. In many respects, their investment into autonomous orbital defense and national security space validates the size and strategic importance of the market. Defense customers are unlikely to commit billions of dollars toward orbital defense architecture unless they believe these capabilities will become foundational to future military infrastructure.

Importantly, True Anomaly’s differentiation appears to be centered around speed, autonomy-first software architectures, rapid spacecraft iteration, and startup-style operational agility, areas where large incumbents have historically struggled. The company’s ability to move quickly, iterate hardware in months rather than years, and align closely with emerging operational doctrines may allow it to capture programs that prioritize adaptability over legacy procurement structures.

Industry Overview

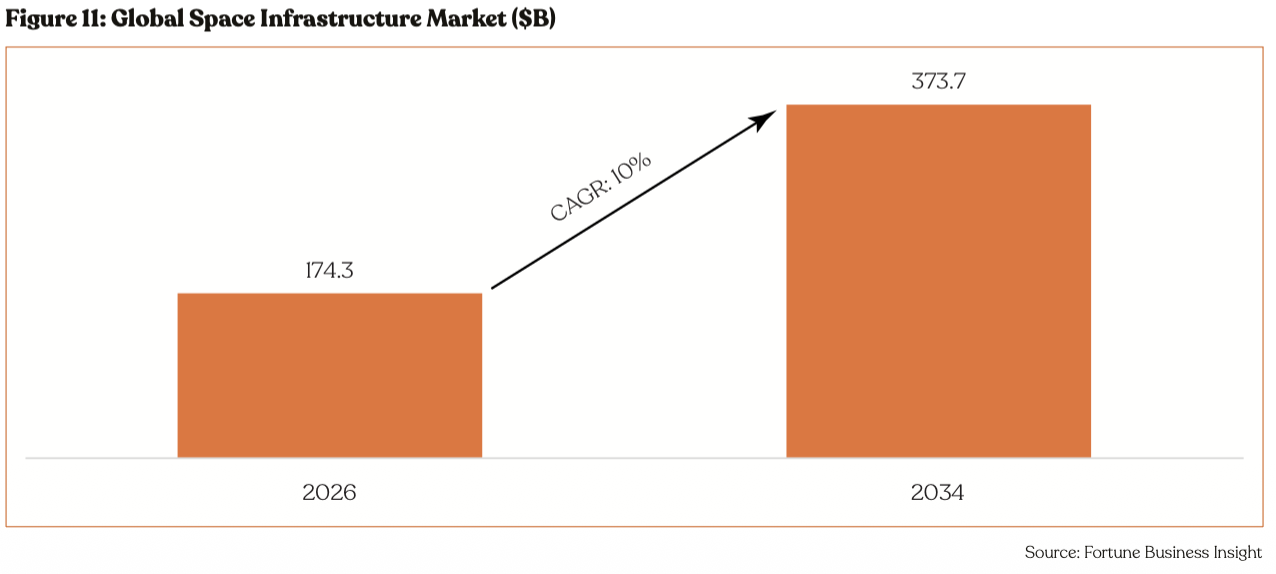

True Anomaly operates within the broader global space infrastructure market, which is projected to grow from $174.3 billion in 2026 to $373.7 billion by 2034, at a CAGR of 10%, per Fortune Business Insights. North America dominated the market with a share of 46.4% in 2025.

Space infrastructure comprises the facilities, technologies, and systems that enable activities in outer space. As a foundational component of the global space economy, the market includes public and private organizations developing and delivering space-enabled products and services.

Investment in space infrastructure is critical to expanding capabilities across telecommunications, navigation, weather forecasting, scientific research, and defense applications. Growing demand for space-based services is accelerating the need for resilient and scalable orbital infrastructure, which underpins operational efficiency, innovation, and long-term growth across the broader space economy.

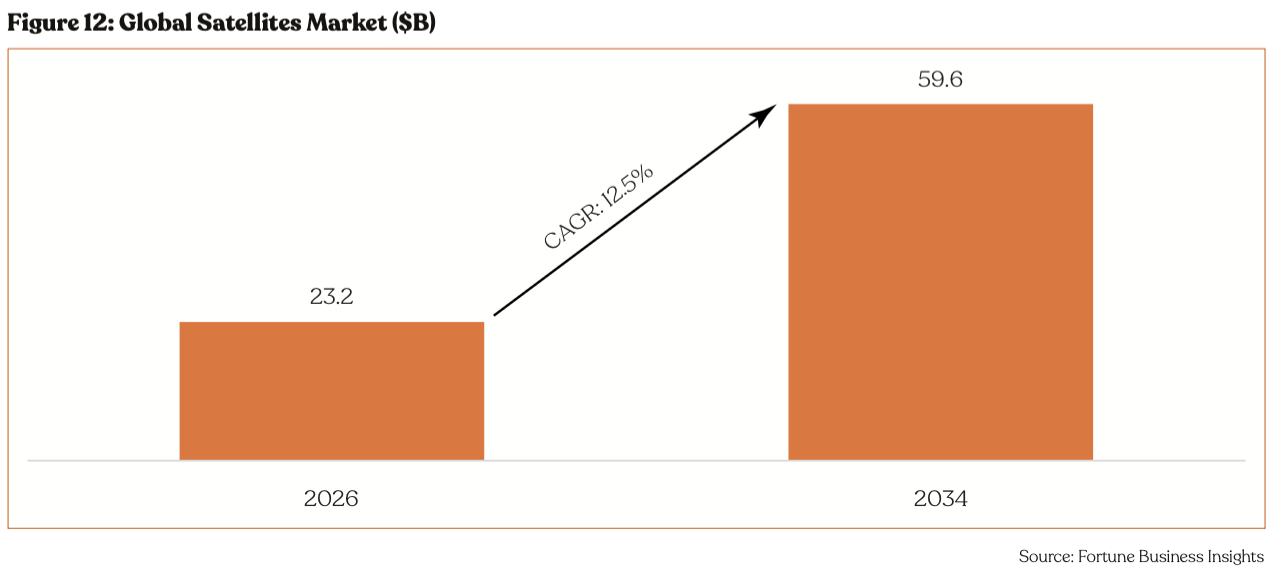

Jackal, the AOV offered by True Anomaly falls within the global satellites market, a core segment of the space infrastructure ecosystem, which is projected to grow from $23.2 billion in 2026 to $59.6 billion by 2034, at a CAGR of 12.5%, per Fortune Business Insights.

The satellites market is a critical enabler of the global space economy, supporting communications, navigation, Earth observation, scientific research, and national security operations. Satellites provide the backbone for real-time connectivity, geospatial intelligence, climate monitoring, and positioning services that support modern digital infrastructure.

Advancements in satellite miniaturization, reusable launch technologies, and onboard processing are reshaping deployment economics and reducing launch barriers. The market spans multiple satellite classes, orbital regimes, components, and end-use applications, serving both commercial and government customers. Increasing adoption of satellite-enabled solutions across telecommunications, defense, agriculture, transportation, and disaster management continues to strengthen long-term market demand and reinforces the strategic importance of space-based infrastructure.

The US remains the global leader in the satellites market, driven by strong commercial innovation, defense modernization initiatives, and continued leadership in space technology development. US operators deploy satellites across communications, Earth observation, navigation, and national security missions, supported by a mature launch ecosystem, robust private investment, and government-backed space programs. Key industry priorities include large-scale satellite constellations, advanced payload integration, and secure communications architectures. Defense and intelligence agencies continue to invest in resilient satellite networks and space-based surveillance capabilities, while commercial operators expand broadband and data services through LEO constellations.

Key industry trends include the rapid adoption of constellation-based deployment models and increasing launch frequency. Small satellites, including nanosatellites and microsatellites, are gaining traction due to their lower cost, shorter development cycles, and operational flexibility. Simultaneously, the expansion of LEO constellations is enabling global broadband coverage and real-time data delivery. Advances in propulsion systems, power management, and onboard computing are further improving satellite performance, mission flexibility, and lifespan.

However, the industry faces growing challenges related to space debris and orbital congestion. Rising satellite density is increasing collision risk and operational complexity, while debris mitigation and end-of-life disposal requirements are adding cost and design constraints. Operators are increasingly required to invest in space situational awareness, collision avoidance systems, and responsible orbital management practices. Failure to address congestion and debris risks could undermine mission safety and long-term sustainability, making coordinated international governance and mitigation efforts critical to the future viability of satellite operations. Enters True Anomaly, a startup well-equipped to tackle these issues. Consequently, True Anomaly raised $600M in Series D funding in April 2026, underscoring investor confidence in the startup.

Beyond mitigating unintentional orbital threats, True Anomaly is also positioned to address intentional and adversarial threats in space. The US Space Force is advancing its SBI program, aimed at deploying a constellation of satellites capable of detecting, tracking, and neutralizing advanced missile threats mid-flight. The program, part of the broader Golden Dome initiative, has awarded contracts worth up to $3.2 billion to companies including True Anomaly, Anduril, and SpaceX.

Traditional defense systems are currently misaligned with the reality of modern warfare. Recent conflicts have exposed the limits of legacy air defense. Highly maneuverable and fast missiles have been able to overwhelm traditional missile defense systems like Iron Dome, Patriot, and THAAD. In March 2026, Iran destroyed a $300 million radar system that directed US missile defense, signaling a need for better solutions.

“Adversaries have invested in exotic, highly maneuverable vehicles [missiles], introducing considerable challenges to protecting the US homeland,"

- Gokul Subramanian, Anduril’s Senior Vice President of Engineering

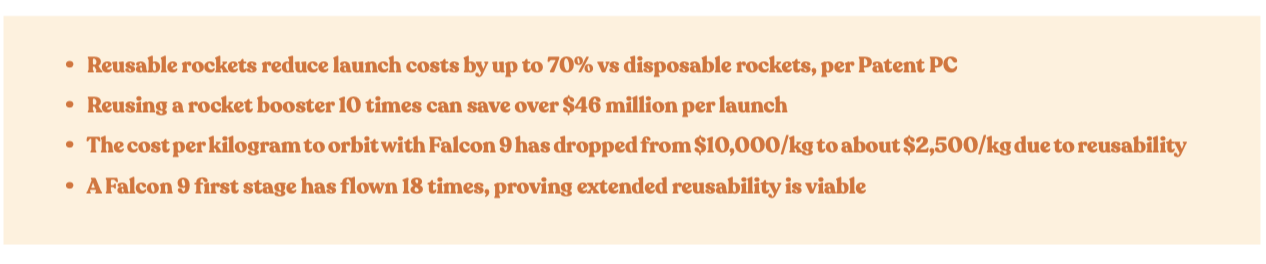

The SBI program is well positioned to address these challenges. Key tailwinds include a 70% reduction in space launch costs and the growing strategic importance of protecting high-value AI infrastructure. Modern AI data centers now require more than $1 billion in capex per facility, making them critical national assets. Recent drone strikes on hyperscale cloud infrastructure in the UAE and Bahrain disrupted banking and enterprise systems, underscoring rising vulnerabilities. Escalating geopolitical threats further strengthen the case for investment in space-based interception systems.

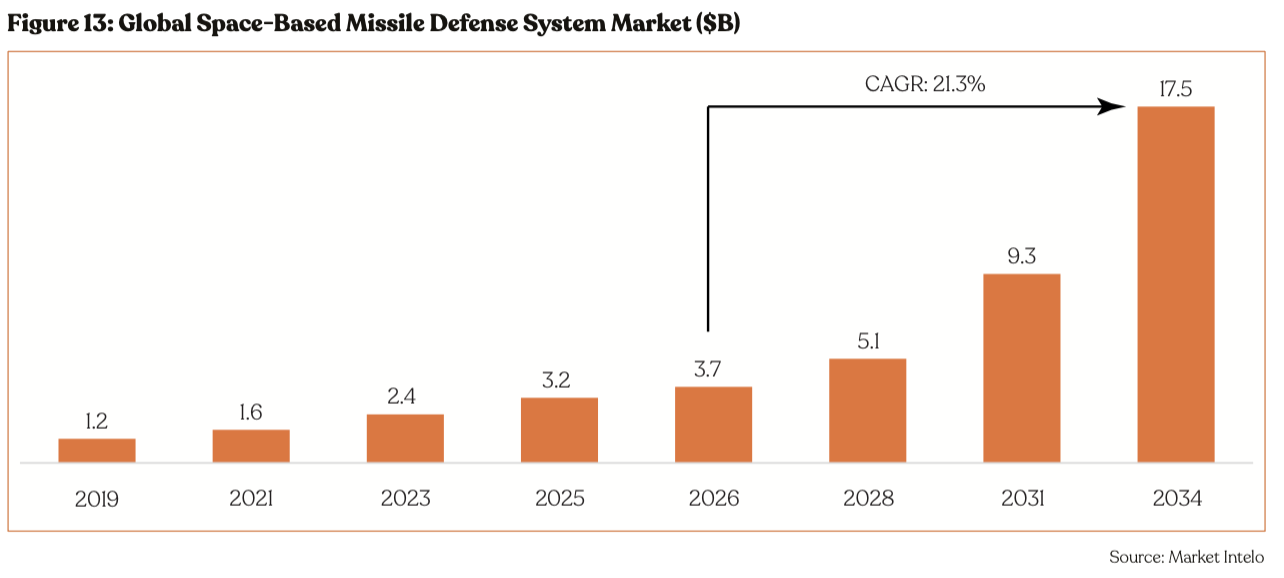

The broader defense technology market is also seeing accelerated capital inflows. National security-focused startups raised $46.3 billion across ~1,900 deals in 2025, representing nearly 900% growth over the past decade, per Pitchbook. Moreover, the global space-based missile defense system market is projected to grow from $3.7 billion in 2026 to $17.5 billion in 2034 at a CAGR of 21.3%, per Market Intelo.

Against this backdrop, True Anomaly is emerging as a potentially high-value strategic asset. Unlike peers that combine defense and commercial space operations, the Colorado-based company is a pure-play space defense platform. The company is vertically integrated, designing and manufacturing spacecraft, software, and mission payloads in-house.

Financials

Revenue Outlook

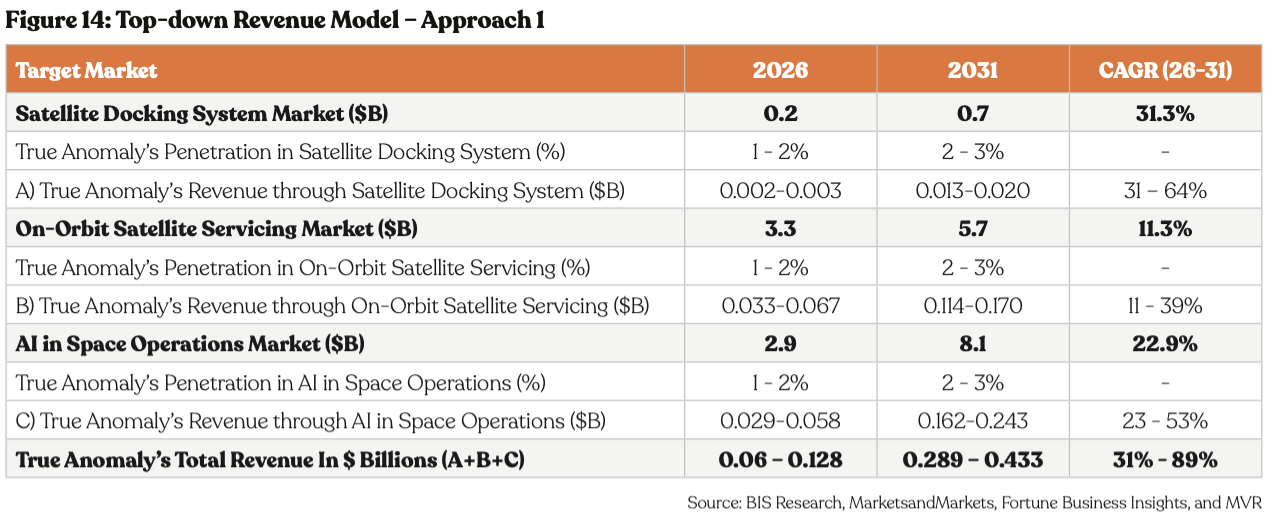

The projections presented here are intended as directional estimates for understanding the potential scale of opportunity True Anomaly could capture by 2031. They offer a framework to think about how the need for intricate space operations may evolve and where True Anomaly’s business could position itself within that trajectory. The market share percentages are subjected to our view of the industry.

The global satellite docking system market is projected to expand from roughly $o.2 billion in 2026 to about $0.7 billion by 2031 at a CAGR of 31.3%, extrapolating data provided by BIS Research. Additionally, the global on-orbit satellite servicing market is projected to grow from roughly $3.3 billion in 2026 to $5.7 billion by 2031, extrapolating data provided by MarketsandMarkets. Moreover, the global AI in space operations market is projected to grow from $2.9 billion in 2026 to $8.1 billion by 2031, extrapolating data provided by Fortune Business Insights.

Assuming True Anomaly secures a 1-2% share of these markets by 2026, rising to 2%–3% by 2031, its revenues could fall in the range of $64–$128 million in 2026 and $289–$433 million in 2031.

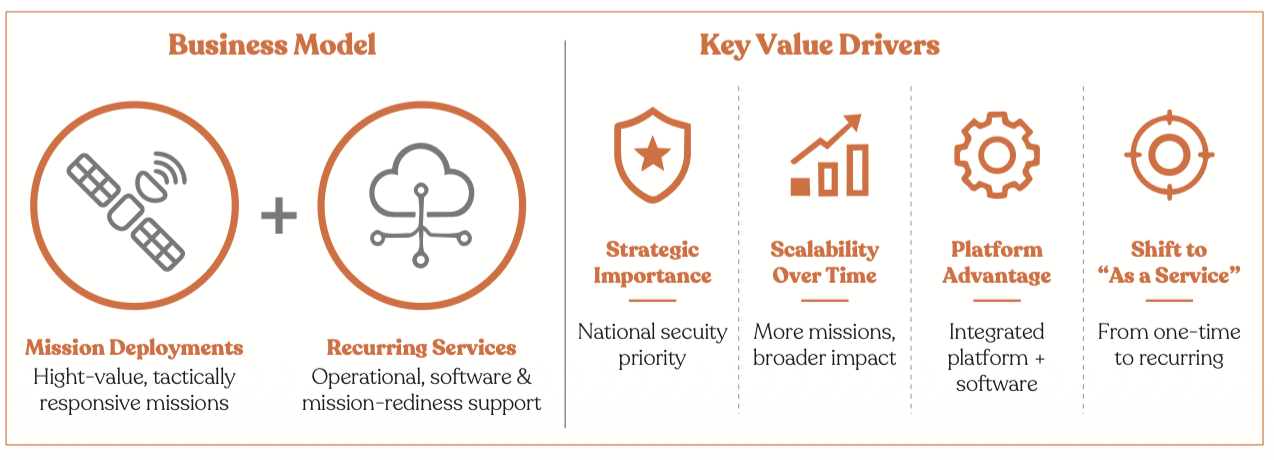

We can also estimate True Anomaly’s revenue across two layers: new mission deployments and recurring orbital-security services. The company’s early revenue is likely driven by bespoke government missions such as VICTUS HAZE, where True Anomaly won a $30M Space Force contract for a Jackal-enabled tactically responsive space mission. Over time, the model can shift from one-off mission awards to a more scalable “space security as a service” model, where governments pay for persistent monitoring, rendezvous/proximity operations, threat characterization, training simulations, and rapid-response readiness.

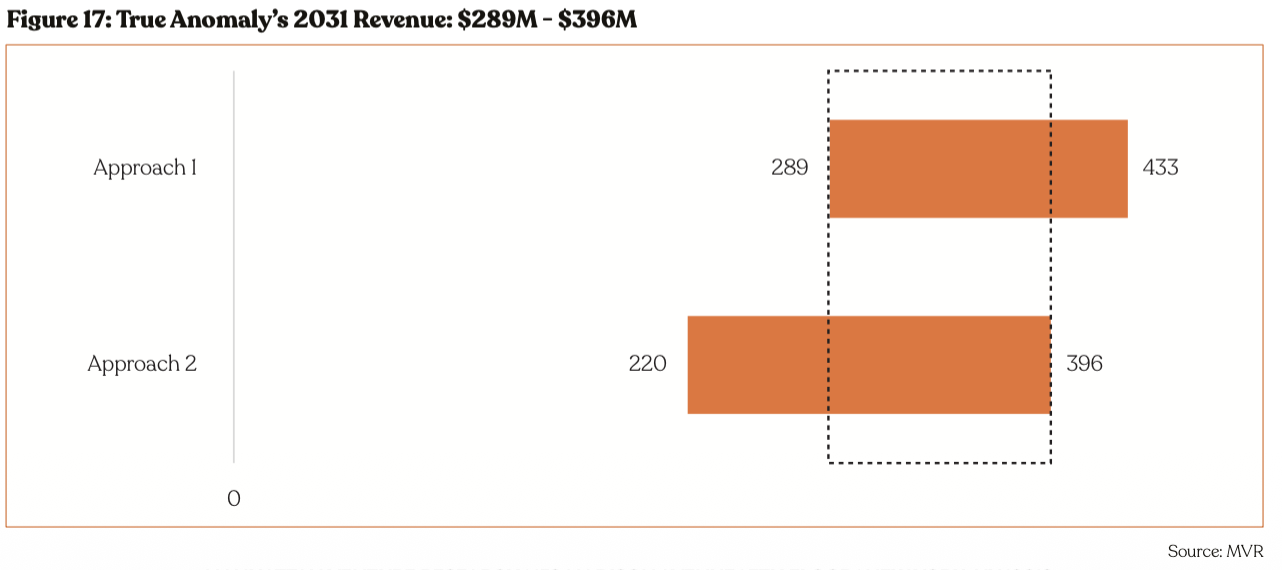

True Anomaly’s revenue potential is best viewed through a multi-layered defense platform model rather than a traditional satellite manufacturing model. In the near term, revenue is likely to be anchored by mission-specific government contracts, with VICTUS HAZE providing an early benchmark at roughly $30M per mission. Over time, as Jackal vehicles mature and Mosaic becomes embedded into space-domain awareness workflows, the company can expand into recurring software, simulation, mission-readiness, and orbital operations revenue. This creates a path from lumpy project-based revenue toward a higher-quality recurring defense-services model, with total revenue potentially scaling from $55-$116 million in 2026 to $220-$396 million by 2031.

Implied Private Market Valuation

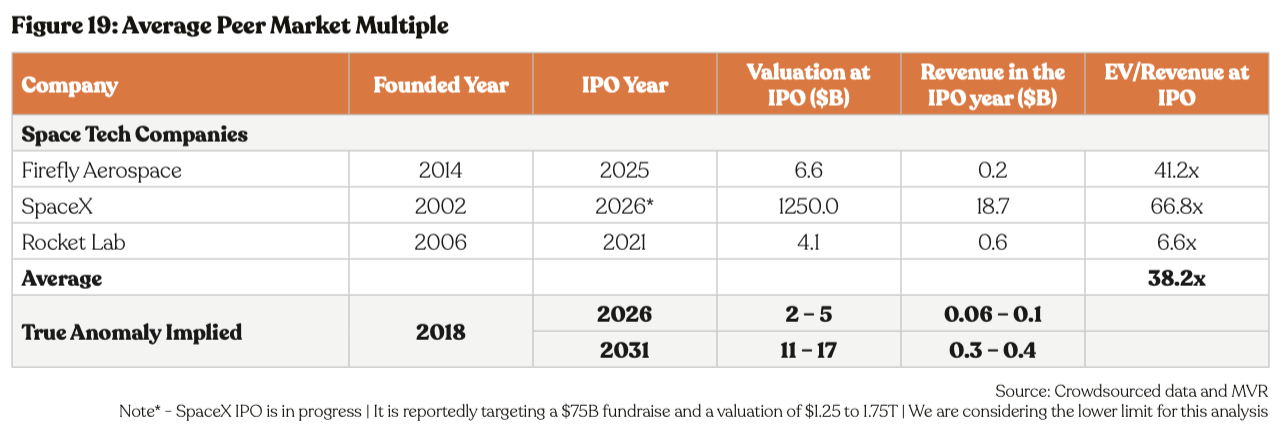

True Anomaly currently lacks direct public market comparable; however, parallels can be drawn from established space tech companies that have accessed public capital markets.

Among the most relevant comparable are Firefly Aerospace, SpaceX (IPO pending), and Rocket Lab. At the time of their respective initial public offerings, these companies were valued at $6.6 billion (Firefly Aerospace), $1,250 billion (SpaceX), and $4.1 billion (Rocket Lab). Their annual revenues at that time were roughly $0.2 billion, $18.7 billion, and $0.6 billion, respectively. These figures yield EV/Revenue multiples of 41.2x, 66.8x, and 6.6x. Averaging across these three data points produces an implied EV/Revenue multiple of approximately 38.2x.

Applying this to True Anomaly’s revenue projections (MVR estimates), a valuation range of $11 billion to $15 billion is achieved for 2031. In this context, an investment in True Anomaly today could be roughly 5x-7x by 2031, based on the current valuation of $2.2 billion.

Potential Strategic Acquisition Value: Large defense primes such as Lockheed Martin, Northrop Grumman, or RTX may eventually require advanced autonomous orbital capabilities to remain competitive. Acquiring a company like True Anomaly could become strategically attractive if internal innovation at traditional defense firms lags next-generation space warfare requirements.

Funding Rounds & Private Valuations

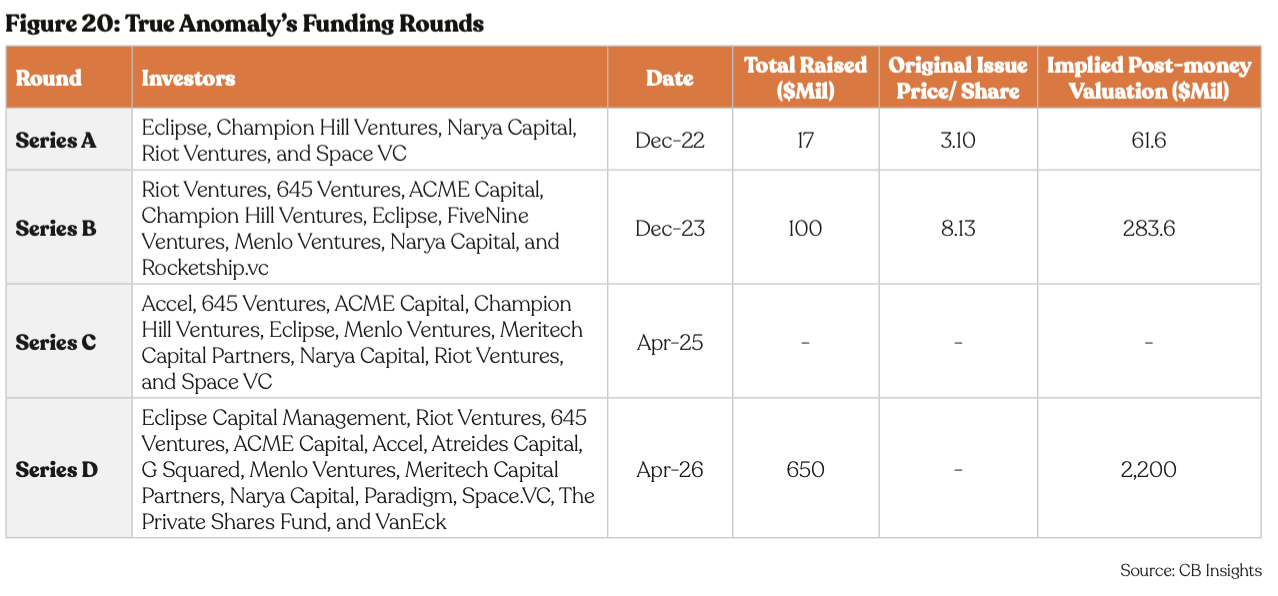

True Anomaly has secured $1 billion in funding across five funding rounds. True Anomaly’s arsenal of highly maneuverable, payload agnostic, and low-cost satellites coupled with complete software stack for space missions has attracted both customers and investors, leading to significant investor interest since 2023. Notably, the company raised $100 million in 2023. The company's ability to attract investment has continued to grow, with its latest funding round, a $650 million series D in April 2026 with, Eclipse Capital Management, Riot Ventures, 645 Ventures, ACME Capital, Accel, Atreides Capital, G Squared, Menlo Ventures, Meritech Capital Partners, Narya Capital, Paradigm, Space.VC, The Private Shares Fund, and VanEck, as investors. The latest funding round valued the company at $2.2 billion.

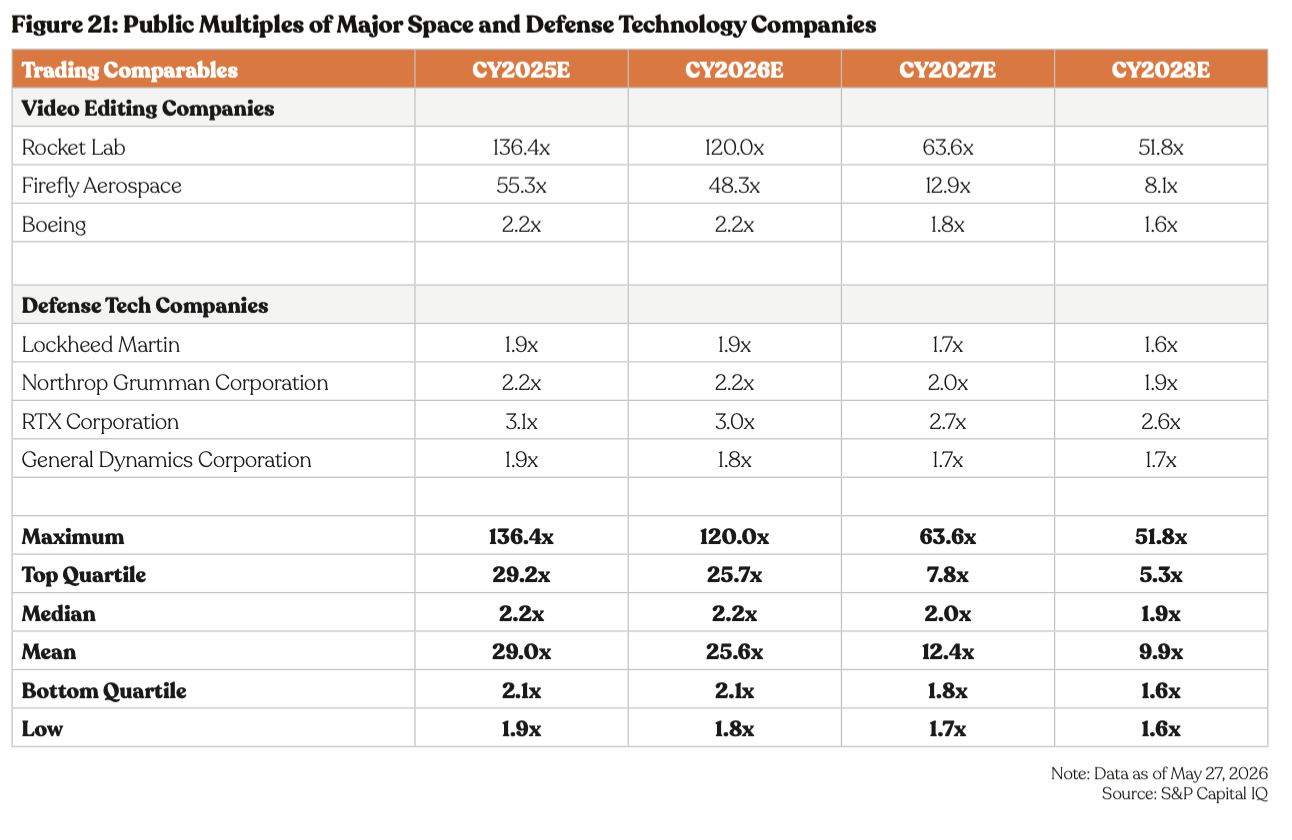

Comparative Public Multiples

The table below shows valuation multiples for public companies in space and defense technology. These public multiples provide a useful reference point for True Anomaly’s future valuation. Given True Anomaly’s purpose-built orbital vehicles and software, designed for space-to-space operations at significantly lower cost than legacy systems, it is reasonable to expect the company to command a premium over its public peers.

About Manhattan Venture Partners

Our Research Methodology

Manhattan Venture Research provides clients with accurate, timely, and innovative research into the companies and sectors we cover. To that end, we have established an experienced team of analysts, researchers, economists, and industry veterans that focus exclusively on private companies with a proven track record of success. Producing quality research on a private company is uniquely challenging. Our analysts communicate with ex-employees, early investors, VCs, competitors, suppliers, and others to gather valuable information about the company under coverage. This information enables us to create unique financial models that value the underlying company and provide insight to our clients and industry experts, leveraging years of experience working for bulge bracket firms. Manhattan Venture Research reports include business and financial aspects of late-stage companies. These reports include but are not limited to industry overviews, competitor analysis, SWOT analysis, products (existing and in development), management and key directors, risks and concerns, other proprietary channels, historical financials, revenue projections, valuations (using various matrices and valuation recommendation), waterfall analysis, and a capitalization table.

Information Access Level Classification System (IALCS)

Manhattan Venture Research uses an Information Access Level Classification System (IALCS) to make clear the degree of access offered by the company(s) covered in all research reports.

Each research report is classified into one of three categories depending on its classification. The categories are:

I++: The company covered by the research report provided substantial disclosures to Manhattan Venture Partners.

I+: The report was prepared following partial disclosure by the company, including publicly available financial statements, and/or is based on conversations with past or present company employees.

I: All reports are prepared using a mosaic research approach. Not all companies are willing and able to provide substantive access to management and information. In I reports no direct access was granted.

About the Analyst

antosh Rao has over 25 years of experience in equity research with a primary focus on the technology and telecom sectors. He started his equity research career at Prudential Securities and later moved to Dresdner Kleinwort Wasserstein, Gleacher & Co, and Evercore Partners, where he followed Telecom and Data Services. Prior to joining Manhattan Venture Partners, he was the Managing Director and Head of Research at Greencrest Capital, focusing on private market TMT research. Santosh has an undergraduate degree in Accounting and Economics, and an MBA in Finance from Rutgers Graduate Business School. While at Gleacher & Co he was ranked leading telecom equipment analyst by Starmine/Financial Times

Disclaimer

I, Santosh Rao, Head of Research, certify that the views expressed in this report accurately reflect my personal views about the subject, securities, instruments, or issuers, and that no part of my compensation was, is, or will be directly or indirectly related to the specific views or recommendations contained herein.

Manhattan Venture Research is a wholly-owned subsidiary of Manhattan Venture Holdings LLC (“MVP”). MVP may currently and/or seek to do business with companies covered in its research report. As a result, investors should be aware that the firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision. This document does not contain all the information needed to make an investment decision, including but not limited to, the risks and costs.

Additional information is available upon request. Information has been obtained from sources believed to be reliable but Manhattan Venture Research or its affiliates and/or subsidiaries do not warrant its completeness or accuracy. All pricing information for the securities discussed is derived from public information unless otherwise stated. Opinions and estimates constitute our judgment as of the date of this material and are subject to change without notice. Past performance is not indicative of future results. MVP does not engage in any proprietary trading or act as a market maker for securities. The user is responsible for verifying the accuracy of the data received. This material is not intended as an offer or solicitation for the purchase or sale of any financial instrument. The opinions and recommendations herein do not take into account individual client circumstances, objectives, or needs and are not intended as recommendations of particular securities, financial instruments, or strategies to particular clients. The recipient of this report must make its own independent decisions regarding any securities or financial instruments mentioned herein. Periodic updates may be provided on companies/industries based on company-specific developments or announcements, market conditions, or any other publicly available information.

Copyright 2025 Manhattan Venture Research LLC. All rights reserved. This report or any portion hereof may not be reprinted, sold, or redistributed, in whole or in part, without the written consent of Manhattan Venture Research. Research is offered through VNTR Securities LLC.

What’s a Rich Text element?

Heading 3

Heading 4

Heading 5

The rich text element allows you to create and format headings, paragraphs, blockquotes, images, and video all in one place instead of having to add and format them individually. Just double-click and easily create content.

Static and dynamic content editing

A rich text element can be used with static or dynamic content. For static content, just drop it into any page and begin editing. For dynamic content, add a rich text field to any collection and then connect a rich text element to that field in the settings panel. Voila!

How to customize formatting for each rich text

Headings, paragraphs, blockquotes, figures, images, and figure captions can all be styled after a class is added to the rich text element using the "When inside of" nested selector system.