Venture Bytes #125: Battery Supply Chain is America’s Achilles’ Heel

Battery Supply Chain is America’s Achilles’ Heel

The US battery industry has fallen dangerously behind China, and the consequences go far beyond economics. Energy security, industrial resilience and, most importantly, national defense now depend on a supply chain America doesn’t control.

The US spent seventy years building energy independence around oil, controlling the infrastructure, logistics, and refining capacity that turned oil into a strategic strength. That control gave it resilience through wars, recessions, and energy shocks.

Today, that energy foundation is changing with batteries emerging as the critical layer of energy security. They will not only propel electric vehicles (EVs), but also power data centers, defense drones, and industrial robots – the systems that define modern competitiveness. But the US enters this new era without control of the supply chain that defines it.

A recent report from the Foundation for Defense of Democracies (FDD) underscores the magnitude of challenge that China's stranglehold on the advanced battery supply chain represents to the US national security and economic interests. The US can’t afford to run its systems of strategic importance on materials which rely on imports from China. Military drones running on foreign batteries is indefensible. In September 2022, the F-35 fighter jet program was briefly halted when a magnet inside its engine was found to contain a Chinese-produced alloy of samarium and cobalt. It was a small part, but a big reminder that even the world’s most advanced systems are vulnerable to reliance on rival-sourced materials.

China’s dominance across every stage of the value chain for current-generation lithium-ion battery technologies is monumental. China makes 80% of the world’s lithium-ion batteries, 85% of the world’s lithium-based anodes and 70% of the cathodes. Beijing also makes 90% of the materials used in those cathodes and 97% of the material for anodes. They process 80% of the world’s lithium, 85% of the world’s battery-grade cobalt, and 95% of the world’s battery-grade graphite.

Modern weapons systems such as unmanned aerial vehicles (UAVs), tactical vehicles, ground equipment, and next-gen soldier electronics all depend on high-density lithium-ion batteries. The US Department of Defense (DoD) currently purchases an estimated 500-700 MWh of rechargeable batteries per year, with rising demand as military systems electrify and unmanned platforms like drones proliferate. The Pentagon has flagged battery supply chain dependence on China as an acute risk, and recommended prioritizing domestic CAM production. A report from defense software firm Govini suggested that nearly 80% of the Defense Department’s weapons systems rely on critical minerals, including those needed for batteries. Outside dependencies of the components of these batteries create unacceptable risks for the military and critical infrastructure.

“Batteries will be the bullets of the future given their increasingly essential role in military and consumer technology” -Elaine Dezenski, Senior Director and Head, Center on Economic and Financial Power at the FDD.

The US has to move quickly on building domestic battery supply chain. The 2024 National Defense Authorization Act prohibits the DoD from procuring batteries containing Chinese-sourced materials beginning October 2027, a deadline that the Pentagon currently lacks domestic capacity to meet. As Deputy Defense Secretary Kathleen Hicks emphasized in the DoD's 2023-2030 Lithium Battery Strategy, "China presently dominates that supply chain," and current US dependence on adversarial sources creates unacceptable risks for military systems.

Battery demand isn’t just a defense story but an economy-wide one. Global demand for lithium-ion batteries is projected to skyrocket from roughly 700 GWh in 2022 to around 4.7 TWh by 2030, according to McKinsey. The US will account for a significant share of this growth, driven by the electrification of transport, industry, and data infrastructure.

Despite record investments, America still finds itself on the back foot in the global battery race. Over the past two years, the US investments in batteries and critical minerals refining have tripled, with more than $40 billion poured into new battery manufacturing facilities between mid-2023 and mid-2024. Much of this momentum comes from the Inflation Reduction Act, whose manufacturing and investment tax credits have triggered a surge of private capital and onshoring announcements. Pentagon has also readied new battery strategy amid growing drone demands, which it plans to release in early 2026.

But the mainstream narrative of building more giga factories misses the deeper issue – vertical integration at the material layer. A battery is only as sovereign as its supply chain. One can assemble a million cells in Michigan, but if the CAM comes from Shenzhen, the security problem is still unsolved. It just moves the choke point upstream and makes it less visible.

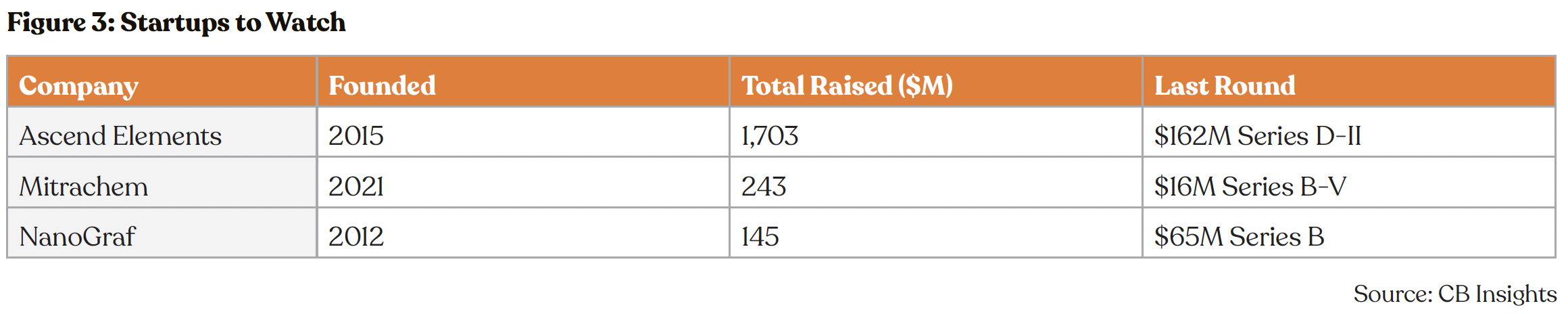

The US battery deficit remains a national vulnerability. As a result, venture-backed firms are stepping up to bridge this gap. Ascend Elements is arguably the most strategically important private battery materials company in the US. It takes end-of-life batteries and scrap and refines them into pCAM (precursor cathode active material) and CAM at commercial scale, closing the loop that the US. never built. Its Apex 1 facility in Kentucky, backed by a $480 million DOE grant and over $700 million in private capital, will supply cathode material for hundreds of thousands of EVs annually. That same midstream capacity can serve defense needs, reducing exposure to China and shortening logistics tails.

Mitra Chem, meanwhile, is leading the US push into iron-based cathodes, specifically LMFP (lithium manganese iron phosphate), a chemistry that’s safer, cheaper, and free of nickel and cobalt. The company’s AI-driven materials platform accelerates discovery and qualification cycles, bringing new formulations to production in months, not years. Its $60 million Series B led by GM underscores how industrial and defense interests are starting to converge around domestic chemistries.

Based in Illinois, NanoGraf manufactures silicon-based anode materials for lithium-ion batteries, replacing traditional graphite anodes to deliver 50-100% increased battery runtime and 15% longer operational life. The company has secured over $45 million in Department of Defense contracts since 2012. The military serves as a proving ground for their silicon anode technology, with batteries delivering 15% longer life than current military standards and supporting up to 25 pounds of battery equipment per soldier mission.

Another key start-up, 6K Energy develops advanced materials using proprietary UniMelt microwave plasma technology, producing metal powders for additive manufacturing and battery cathode active materials for energy storage applications. The Massachusetts-based company has secured $123.4 million in government grants from the Department of Energy and Department of Defense since 2022. The company’s government contracts with NASA, Lockheed Martin, and Firefly Aerospace demonstrate focus on mission-critical applications.**

AI Scribe is Healthcare’s Most Urgent Fix

The race to dominate AI-powered medical scribing is accelerating. The US healthcare industry, historically a laggard in software adoption, is now the fastest adopter of enterprise AI. It is deploying AI at more than 2.2x the rate of the broader economy, according to Menlo Ventures.

The reason is simple and urgent. Healthcare’s labor model is collapsing under its own administrative weight. Physicians spend nearly as much time on documentation, coding, and EHR tasks as they do on actual patient care, and the system has run out of human capacity to absorb the load.

And while many parts of healthcare are ripe for AI transformation, medical scribing stands out as one of the most urgent and high-impact areas.

American physicians spend more than one-third of their workweek on documentation. These hours are lost to the administrative black hole that has swallowed the modern healthcare system. This administrative load on healthcare providers often overshadows the time and energy dedicated to direct patient care and is a major contributor to physician burnout.

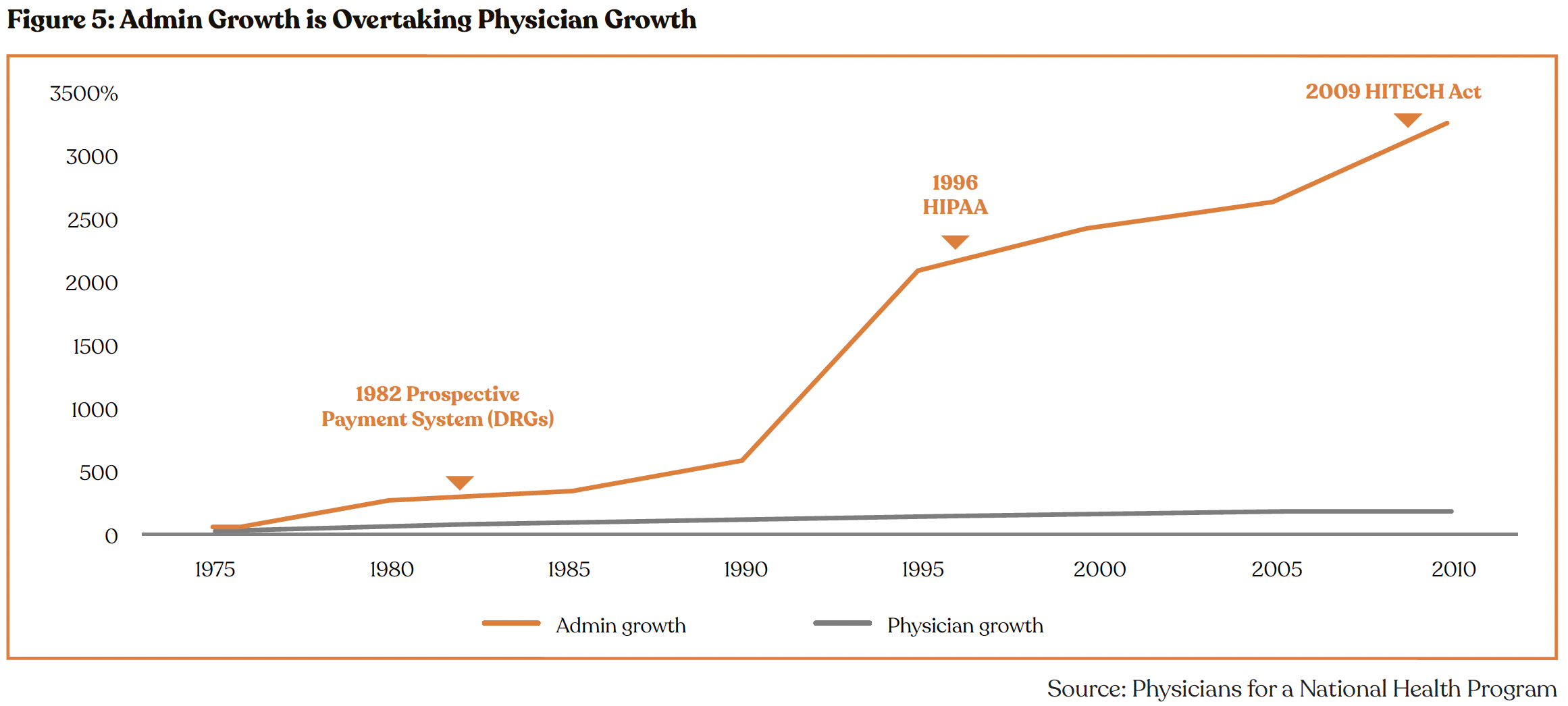

The number of physicians in the US grew 150% between 1975 and 2010, according to Physicians for a National Health Program using data from the Bureau of Labor Statistics, the National Center for Health Statistics, and the United States Census Bureau's Current Population Survey. In contrast, healthcare admin professionals grew 32,00%. While this specific data is from 2010, the broader trend persists. The supply of patient-care physicians per capita rose by only 9.3% between 2009 and 2019 (from 25.8 to 28.2 per 10,000 residents), according to the CDC, indicating that the administrative workload continues to outpace clinical capacity.

As of 2023, national health expenditure was $4.9 trillion in 2023, per the US Centers for Medicare & Medicaid Services. Various studies over the last 2 decades have found that administrative expenses account for approximately 15% to 25% of total national health care expenditures. Based on this, this is $750 billion - $1.2 trillion in total administrative spending annually. A significant portion of that cost is tied to clinical documentation and corresponding revenue cycle workflows-tasks that are increasingly pushed onto clinicians. These processes demand accurately capturing granular details from clinical conversations, translating them into the thousands of evolving billing codes (such as ICD-10, CPT), and navigating payer-specific documentation requirements.

There are around 100,000 human medical scribes in the US (per Perspectives in Health Information Management estimates), who earn ~$35,000/year, suggesting that the medical scribe market alone represents a $3.5B+ wedge. However, the actual market opportunity could be much bigger across administrative workflow including revenue cycle management, coding, and prior authorization.

“These (AI scribes) are set to become a commodity in the coming years," – Sara Murray, Vice President, Chief Health AI Officer for UCSF Health.

The adoption curve for AI scribe tools is already steep and accelerating. Across major US health systems, ambient scribing is moving from experiment to default workflow. Kaiser Permanente reports that 65–70% of its physicians are now using elements of Abridge’s AI scribe. At UCSF, 800 of 2,000 eligible ambulatory providers are using such tools. UC Davis Health shows similar traction with 350 of 800 ambulatory physicians using Abridge and roughly 100 new clinicians added every month. Even large, complex systems like Providence, historically slower adopters, now have 1,700 out of 6,500 eligible providers using Microsoft’s ambient scribe in outpatient care, with expansion underway to ER clinicians, advanced practitioners, and inpatient teams next.

The speed and convenience of deployment are other key reasons adoption is spreading this quickly. Unlike traditional healthcare software, which often requires quarters (or years) of training, configuration, and workflow change, AI scribes can scale from pilot to full implementation in a matter of months. At UC Davis, Abridge onboarding requires 11 minutes of training, a stunning contrast to the multi-hour or multi-day sessions clinicians endure for EHR updates.

In addition to AI scribes, high-impact adjacencies exist in data-rich clinical workflows where AI can directly improve outcomes. Clinical trial patient recruitment and matching accelerates drug development timelines by automatically identifying eligible participants from EHR data. These workflows unlock billions in trapped pharma R&D value and create durable defensible moats through proprietary trial datasets.

Vision-based clinical analysis into radiology, pathology, and diagnostic imaging represents an even larger market, capturing 75% of patient encounters through medical imaging. Aidoc, which raised its Series D round earlier this year, runs 15 FDA-cleared algorithms across 3,000+ hospitals.

Healthtech companies with AI scribe capabilities have naturally attracted substantial capital, reflecting the size of the administrative problem they aim to solve. With over $4.8 billion raised since 2019 and $1.6 billion in 2025 alone (as of September, per Pitchbook), the market is aggressively funding the platforms best positioned to navigate the clinical complexities of this space.

Healthtech companies focusing on AI scribe capabilities have attracted enormous capital, with over $4.8 billion raised since 2019 and $1.6 billion in 2025 alone (as of September, per Pitchbook). As the industry matures, venture-growth stage deal size has surged from an average of $150 million in 2021 to $263 million in 2025.

While there are 40+ scribe start-ups in the US, per Pitchbook, few key start-ups have aggressively distinguished themselves. Abridge is widely considered the category leader, having launched its conversation intelligence platform before large language models (LLMs) were household names. This early entry provided the deep clinical training and hospital integration needed to build a durable platform. The company recently secured a massive $300 million Series E round, achieving a $5.3 billion valuation. Abridge’s AI scribe technology is already trusted by over 150 of the largest health systems in the US, cementing its enterprise scale. In 1Q25, the company reached $117 million in contracted annual recurring revenue.

Ambience Healthcare is positioning itself as an end-to-end ambient AI platform, aiming for comprehensive coverage across documentation, coding, and clinical documentation integrity. This full-stack approach makes it a powerful choice for large, complex health systems seeking holistic solutions. The company serves prestigious large healthcare organizations like Cleveland Clinic, Houston Methodist, UCSF Health, and Ardent Health. Top-tier venture firms like Andreessen Horowitz, Kleiner Perkins, Optum Ventures, and the OpenAI Startup Fund have backed Ambience.

Massachusetts-based Eleos Health stands out for its deep specialization in the behavioral and mental health market. The company raised a $60 million Series C in January 2025, with its valuation doubling as it proves the ROI in this niche. Eleos’ AI-powered tools are proven to reduce the time providers spend on documentation by more than 70%. The company serves over 200 organizations with 35,000+ providers across 30+ states.**

What’s a Rich Text element?

Heading 3

Heading 4

Heading 5

The rich text element allows you to create and format headings, paragraphs, blockquotes, images, and video all in one place instead of having to add and format them individually. Just double-click and easily create content.

Static and dynamic content editing

A rich text element can be used with static or dynamic content. For static content, just drop it into any page and begin editing. For dynamic content, add a rich text field to any collection and then connect a rich text element to that field in the settings panel. Voila!

How to customize formatting for each rich text

Headings, paragraphs, blockquotes, figures, images, and figure captions can all be styled after a class is added to the rich text element using the "When inside of" nested selector system.